Most families are told one thing:

“Get life insurance and your family will be protected.”

But protection is not the same as wealth.

And confusing the two is where most families fall behind.

The Misunderstanding Most People Have

Life insurance is often presented as the foundation of financial security.

And to be clear—it serves a purpose.

But it does one primary thing:

It pays out when you die.

That’s not a wealth-building system.

That’s a safety net.

What Life Insurance Actually Does

Life insurance is designed to:

- Replace lost income

- Cover funeral and final expenses

- Provide a payout to beneficiaries

In some cases, policies like whole life or indexed universal life can build cash value.

But even then, the structure is still limited.

You are relying on:

- An external company

- Policy rules you don’t control

- A payout tied to a specific event

It is protection. Not control.

What a Family Bank Actually Does

A family bank is not a product.

It is a system.

It allows a family to:

- Pool capital together

- Lend money internally

- Finance opportunities without outside lenders

- Keep interest circulating within the family

- Build discipline and structure across generations

Instead of money leaving your household…

it stays and grows inside it.

The Real Difference: Control vs Payout

This is where the separation becomes clear.

Life Insurance:

- Pays once (or under specific conditions)

- Controlled by an insurance company

- Limited flexibility

- Reactive (after death or policy triggers)

Family Bank:

- Operates continuously

- Controlled by the family

- Flexible and scalable

- Proactive (used during life)

One protects against loss.

The other builds power.

Why Wealthy Families Use Both

This is where most people get it wrong.

It’s not “either or.”

The most effective strategy is layering both systems.

- Life insurance provides liquidity when needed

- A trust structure protects and directs that money

- A family bank puts that money to work

Now the payout doesn’t just get spent…

It gets circulated.

The Power of Combining the Two

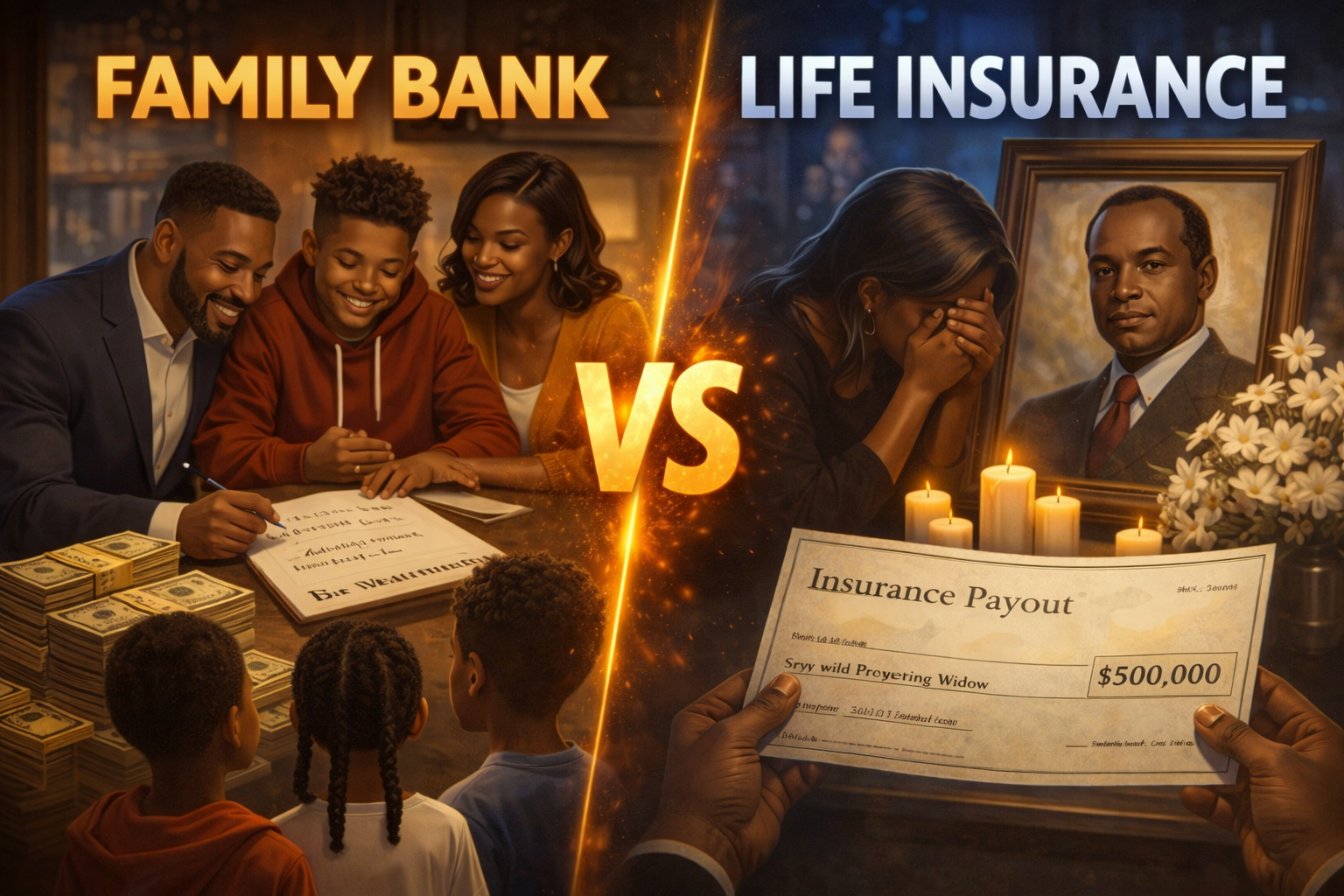

Imagine this:

A life insurance policy pays out $500,000.

Instead of that money being used and gone…

It enters a family bank.

Now that same $500,000 can:

- Fund businesses

- Help family members avoid high-interest debt

- Be loaned and repaid with interest

- Continue growing across generations

That is the shift from inheritance…

to institution.

Where Most Families Go Wrong

Most families:

- Receive money

- Spend it

- Restart the cycle

Without structure, even large payouts disappear.

It’s not about how much comes in.

It’s about what system it enters.

Build the System First

Before worrying about large amounts of money…

Focus on structure.

- How will money be managed?

- Who controls it?

- How is it deployed?

- How is it preserved?

That’s what separates families that build wealth…

from those that briefly touch it.

Start Your Family Bank System

If you want to move from income to structure, this is where it starts.

The Family Bank Starter System shows you how to:

- Set up your internal lending structure

- Create rules and governance

- Build capital step by step

- Keep money circulating inside your family

Get The Family Bank Starter System:

https://stan.store/blackdollarandculture/p/the-family-bank-starter-system

Protect It With the Right Structure

If you’re using life insurance, it needs to be structured properly.

An ILIT (Irrevocable Life Insurance Trust) allows you to:

- Keep payouts outside of your taxable estate

- Control how money is distributed

- Protect the policy from misuse

Get Your Family Wealth Trust Blueprint (ILIT):

https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now

FAQ

Is a family bank better than life insurance?

They serve different roles. A family bank builds and circulates wealth, while life insurance provides protection and liquidity.

Can you start a family bank without a lot of money?

Yes. The system matters more than the starting amount.

Do wealthy families really use this strategy?

Yes. Many wealthy families combine trusts, insurance, and internal capital systems to preserve and grow wealth.

Final Thought

Life insurance can leave your family money.

A family bank can leave your family a system.

And systems are what create generational wealth.

Focus Keyphrase: Family Bank vs Life Insurance

Slug: Family Bank vs Life Insurance

Meta Description: Discover the difference between a family bank and life insurance, and how combining both can build generational wealth, protect assets, and create financial control.