The Hidden Lessons of Rosewood

Most people know Rosewood because of how it ended. Far fewer understand how it lived. The story of Rosewood, Florida, is often remembered for the racial violence of January 1923 that destroyed a once-thriving Black community. The tragedy deserves to be remembered, but focusing only on its destruction overlooks an equally important story—the determination, entrepreneurship, and self-reliance that allowed Rosewood’s residents to build prosperous lives in the decades before the violence. If we study only the town’s final days, we miss the lessons found in the years that came before. The history of Rosewood is not simply a story of loss. It is also a story of resilience, ownership, hard work, and community. A Community Built Through Determination Following the end of slavery, many Black families sought opportunities to build independent lives across the South. Rosewood became one of those places. Residents established homes, purchased land, founded churches, educated their children, and developed businesses that supported the growing community. Although opportunities were often limited by segregation and discrimination, families continued investing in their futures. The lesson remains timeless. Strong communities are often built one family, one home, and one business at a time. Land Was More Than Property For many Rosewood families, land represented security. Owning acreage meant having a place to build a home, raise children, grow crops, harvest timber, or pass something valuable to the next generation. Land created options. It offered independence that renting could not provide. Throughout American history, land ownership has frequently served as the foundation upon which families build long-term wealth. Skilled Work Created Prosperity Rosewood was not sustained by a single industry. Residents worked as farmers, carpenters, laborers, teachers, ministers, craftsmen, and entrepreneurs. Many earned their living through the region’s timber economy while others provided services that every growing town required. Prosperous communities depend upon people with different skills working together. Economic strength is rarely built by one profession alone. Churches Became Community Anchors Churches served purposes far beyond worship. They became gathering places where families organized, celebrated milestones, supported neighbors during hardship, and strengthened community relationships. In many Black communities throughout the early twentieth century, churches also encouraged education, leadership, and mutual assistance. Strong institutions often strengthen strong communities. Education Was An Investment Parents understood that education could create opportunities unavailable to previous generations. Schools helped prepare children for skilled work, leadership, and professional careers. Knowledge became an investment that no one could easily take away. Generations have demonstrated that education often becomes one of the most valuable assets a family can possess. Neighbors Supported One Another Communities become stronger when trust exists between neighbors. Families shared information. They helped one another during difficult seasons. Local businesses depended upon loyal customers, while customers depended upon dependable business owners. These relationships created social capital alongside financial capital. Trust itself became an economic asset. Wealth Is More Than Money Rosewood reminds us that wealth cannot always be measured by bank accounts alone. A family’s home. A church. Friendships. Knowledge. Land. A reputation for honesty. These forms of wealth helped sustain communities through both prosperity and hardship. Financial assets matter, but so do the relationships and institutions that support them. History Also Teaches Preparedness The destruction of Rosewood remains one of the most painful chapters in American history. Many families lost homes, businesses, personal belongings, and property they had spent years building. The lasting consequences extended well beyond one generation. The tragedy reminds us that preserving records, protecting property rights, maintaining strong family networks, and documenting ownership are important parts of safeguarding a family’s legacy. Legacy Lives Beyond Buildings Although Rosewood itself was destroyed, its story did not disappear. Descendants preserved family histories. Researchers documented the town’s past. Historians continued uncovering records that help tell a fuller story of the people who lived there. Their determination ensured that Rosewood would be remembered not only for tragedy but also for the lives its residents built before 1923. The Greatest Lesson Rosewood teaches that communities are created through ownership, education, skilled work, faith, cooperation, and long-term thinking. Its history reminds us that prosperity requires patience. Homes are built over years. Businesses grow through consistency. Families create legacies by investing in future generations rather than focusing only on the present. Remembering Rosewood means remembering more than its destruction. It means honoring the determination of the families who built something worth preserving. Conclusion The story of Rosewood deserves to be studied not only because of what was taken, but because of what was created. Its residents demonstrated that ownership, education, community, and perseverance could lay the foundation for prosperity even under difficult circumstances. History is most valuable when it helps us understand both the challenges people faced and the principles that helped them succeed. The true lesson of Rosewood is not simply that a town was lost. It is that its legacy continues to remind us why building strong families, strong institutions, and lasting assets still matters today. SEO Title: The Hidden Lessons of Rosewood: What History Teaches About Ownership and Legacy URL Slug: hidden-lessons-of-rosewood Meta Description: Discover the hidden lessons of Rosewood and learn how ownership, land, faith, education, and community built a thriving Black town before 1923. Focus Keyphrase: Hidden Lessons of Rosewood

How One Rental Property Can Change Your Family’s Financial Future Forever

Introduction Many people believe they need dozens of properties, millions of dollars, or years of experience before real estate can make a meaningful impact on their finances. The truth is that for many families, wealth begins with a single property. One rental property may not make you rich overnight, but it can start a financial chain reaction that changes the trajectory of your family for decades. It can create monthly cash flow, build equity, provide tax advantages, and eventually become an asset that can be passed down to future generations. The journey to wealth often starts with one door. The Difference Between Income and Ownership Most families rely almost entirely on earned income. They work.They get paid.They spend.Then the cycle repeats. While employment can provide stability, ownership creates leverage. When you own a rental property, someone else helps pay for an asset that you control. Every rent payment contributes to your wealth-building journey. Instead of relying solely on your paycheck, you now have an asset working alongside you. Rental Income Creates Additional Cash Flow One of the biggest benefits of rental property ownership is monthly cash flow. Imagine owning a property that generates income every month after expenses are paid. That extra income can be used to: Over time, even a few hundred dollars per month can add up to thousands of dollars annually. The goal is not simply earning more money. The goal is creating income streams that do not depend entirely on your labor. Equity Builds Wealth Quietly Every mortgage payment typically contains a principal portion. That means every month you own the property, a portion of the debt is reduced. At the same time, the property’s value may increase over the long term. This creates equity. Equity is one of the most powerful wealth-building tools available because it grows quietly in the background while life continues. Many families underestimate how valuable this can become after 10, 20, or 30 years. Appreciation Can Multiply Your Wealth Historically, real estate has appreciated over long periods of time. While markets move up and down, many property owners benefit from increasing property values over decades. For example: A $200,000 property that grows in value over time may eventually be worth significantly more than its original purchase price. Combined with rental income and loan paydown, appreciation can create a powerful wealth-building formula. One Property Can Lead to Another Many successful investors did not start with ten properties. They started with one. The cash flow and equity from the first property often help fund future opportunities. Property #1 can help purchase Property #2. Property #2 can help purchase Property #3. The process may take years, but wealth often grows through patience and consistency rather than speed. Creating Generational Wealth Perhaps the greatest benefit of rental property ownership is the ability to transfer assets to future generations. Many families inherit bills. Wealthy families often inherit assets. A rental property can provide: When structured properly, a rental property can continue benefiting children, grandchildren, and future generations. Why Ownership Matters The wealthiest families in history have consistently focused on ownership. They own businesses. They own land. They own real estate. Ownership creates opportunities that employment alone often cannot. A rental property may not seem life-changing today, but decades from now it could become one of the most important financial decisions your family ever makes. Final Thoughts One rental property will not solve every financial problem. However, it can create a powerful foundation for long-term wealth. It can generate cash flow, build equity, provide appreciation, and create opportunities for future generations. Many families spend years waiting for the perfect opportunity. The families who build wealth often start with what they can afford and allow time to do the heavy lifting. Sometimes changing your family’s future begins with a single property. Build Your Family Wealth System If you’re serious about protecting your family and building long-term wealth, start here: 🏠 Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 🛡️ Family Wealth Trust (ILIT Blueprint)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now Focus Keyphrase One Rental Property Can Change Your Family’s Financial Future Tags Rental Property, Real Estate Investing, Passive Income, Cash Flow, Generational Wealth, Family Wealth, Financial Freedom, Real Estate, Family Bank, Black Dollar and Culture, Wealth Building, Property Ownership, Rental Income, Investing, Ownership Economics Meta Description Discover how a single rental property can create cash flow, build equity, generate passive income, and help your family create generational wealth. Focus Keyphrase One Rental Property Can Change Your Family’s Financial Future URL Slug one-rental-property-can-change-your-familys-financial-future

Your Job Won’t Make You Rich: The Ownership Secret

For generations, people have been taught a simple formula for success: Go to school. Get a good job. Work hard. Save money. Retire someday. While there is nothing wrong with having a job, many people make the mistake of believing that a job alone will make them wealthy. The truth is that most wealthy families understand a principle that is rarely taught in school: Jobs create income. Ownership creates wealth. A paycheck can help you survive, but ownership can help you thrive. The Trap of Trading Time for Money When you work a job, you are exchanging your time for money. You work eight hours and get paid for eight hours. You work overtime and earn a little more. You stop working and eventually the income stops too. This creates a problem because there are only twenty-four hours in a day. No matter how talented or hardworking you are, your earning potential is often limited by the number of hours you can work. Many people spend forty years climbing a ladder only to discover that they are still dependent on a paycheck. They have income, but they do not have wealth. The Difference Between Income and Wealth Income is money that comes from your labor. Wealth is ownership of assets. An asset is something that puts money into your pocket or grows in value over time. Examples include: The wealthy focus on accumulating assets because assets can continue working even when they are not. That is the power of ownership. Why Wealthy Families Buy Assets Imagine two people. The first person earns $100,000 per year from a job. The second person earns $60,000 from a job but owns rental properties, dividend stocks, and a small business. At first glance, the first person appears more successful. But over time, the second person may build far more wealth because their assets continue generating income year after year. While the worker is earning money from labor, the owner is earning money from ownership. The wealthy understand that assets create leverage. Leverage allows your money to work harder than you can. The Ownership Mindset Ownership begins with a different way of thinking. Instead of asking: “How can I make more money?” Owners often ask: “What can I own?” That simple shift changes everything. Instead of buying liabilities that lose value, owners focus on acquiring assets. Instead of spending every raise, they invest. Instead of consuming, they accumulate. Instead of depending solely on a paycheck, they create additional streams of income. The System Rewards Ownership Take a look around. Many of the world’s wealthiest people are owners. They own companies. They own real estate. They own patents. They own intellectual property. They own brands. They own assets that millions of people use every day. The largest fortunes in history were rarely built from wages alone. They were built through ownership. Ownership provides the opportunity to benefit from the labor, spending, and productivity of an entire marketplace rather than only your own labor. Why So Many People Stay Stuck Most people are never taught how wealth is actually created. They are taught how to earn. They are not taught how to own. As a result, many people spend decades purchasing things that depreciate while neglecting assets that appreciate. Cars get upgraded. Phones get replaced. Clothes go out of style. Yet investment accounts remain empty. Ownership opportunities are ignored. The cycle continues. This is why many people can earn good incomes and still struggle financially. Building Wealth One Asset at a Time The good news is that ownership is not reserved for the rich. Every asset begins with a first step. The first stock purchase. The first rental property. The first side business. The first piece of land. The first investment account. The first digital product. Small assets can grow into large assets over time. The key is consistency. Wealth is often built slowly before it becomes visible. Creating a Family Legacy The most powerful aspect of ownership is that it can extend beyond your lifetime. Businesses can be inherited. Land can be passed down. Investment portfolios can continue growing. Trusts can protect family wealth. Assets can create opportunities for children and grandchildren. A paycheck typically stops when the worker stops working. Ownership can continue producing value for generations. That is why wealthy families focus on building systems, structures, and assets that outlive them. Final Thoughts A job is important. A job can provide stability, security, and opportunities. But if your goal is financial freedom, a paycheck alone is rarely enough. The goal is not to abandon work. The goal is to use your income to acquire assets. The goal is to move from worker thinking to owner thinking. The goal is to build ownership. Because jobs create income. But ownership creates wealth. 📚 Family Bank Starter System 🛡️ Family Wealth Trust Blueprint (ILIT) SEO Information SEO Title:Your Job Won’t Make You Rich: The Ownership Secret Wealthy Families Understand Meta Description:A job can provide income, but ownership creates wealth. Learn why wealthy families focus on businesses, stocks, land, and assets instead of relying solely on a paycheck. Focus Keyphrase:Your Job Won’t Make You Rich URL Slug:your-job-wont-make-you-rich-the-ownership-secret

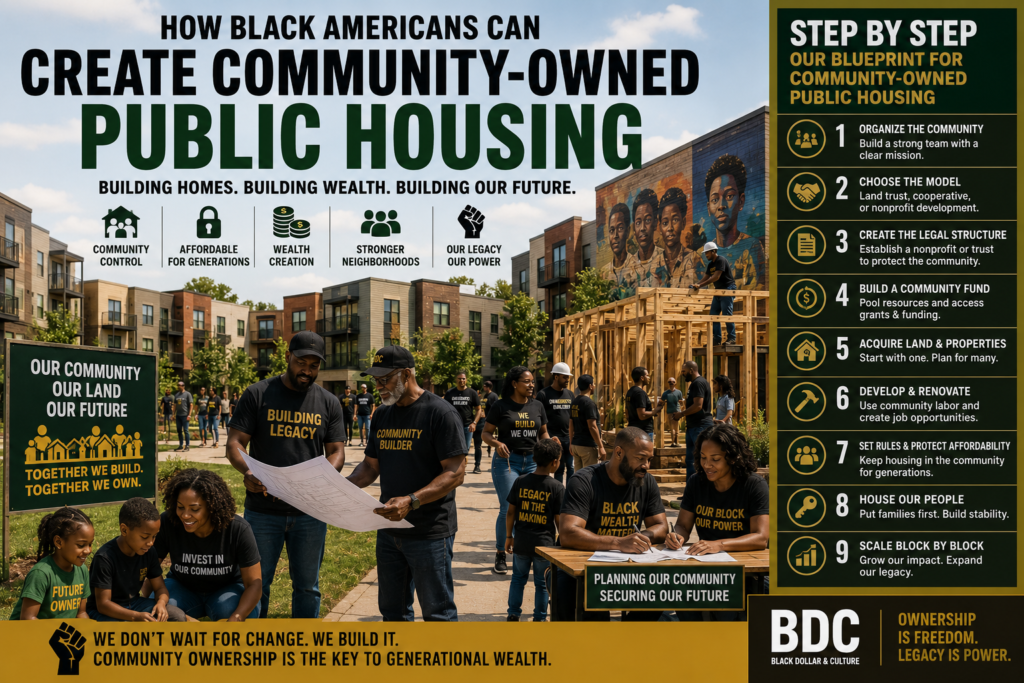

How Black Communities Can Build Public Housing Without Waiting on Government Housing

Housing has always been one of the biggest keys to power in America. Whoever controls the land controls the neighborhood. Whoever controls the neighborhood controls the businesses, schools, safety, rent prices, and future wealth of the people living there. For Black Americans, the housing conversation cannot only be about renting cheaper apartments or waiting for someone else to build affordable housing. We have to think bigger. The real question is: How can we create housing that the community owns, protects, and passes down? This is where community-owned housing comes in. Community-owned housing is when people come together to buy land, build homes, control affordability, and keep property from being taken over by outside investors. It is not just about shelter. It is about ownership, protection, legacy, and economic power. Step 1: Form a Housing Vision Group The first step is gathering the right people. This group should include: Community leaders, church leaders, real estate agents, contractors, electricians, plumbers, attorneys, accountants, business owners, investors, and serious families who care about ownership. This cannot be just a conversation group. It has to become an action group. The mission should be clear: Acquire land, build or renovate homes, and keep housing affordable for Black families and working-class families. Start with 5 to 10 serious people. Not everybody has to have money. Some people may bring skills. Some may bring land. Some may bring credit. Some may bring legal knowledge. Some may bring construction experience. The first goal is organization. Without organization, money gets wasted.Without leadership, ideas die.Without a structure, the community stays dependent. Step 2: Choose the Ownership Model Before buying property, the group must decide how the housing will be owned. There are three strong models. Community Land Trust A Community Land Trust is one of the strongest options. The community owns the land through a nonprofit trust. Families may rent or buy homes on that land, but the land itself stays protected. This keeps outside investors from buying up the neighborhood and raising prices. The land becomes a permanent community asset. Housing Cooperative A housing cooperative means the residents collectively own the property. Instead of paying rent to an outside landlord, residents own shares in the cooperative. They help make decisions, vote on leadership, and share responsibility. This works well for apartments, duplexes, townhomes, or small communities. Church or Nonprofit Housing Development Many Black churches and nonprofits already own land. Some of that land sits unused. That land could become senior housing, starter homes, rental units, tiny homes, duplexes, or family housing. Churches already have trust, leadership, and community connection. If structured correctly, church-owned land can become a powerful housing solution. Step 3: Create the Legal Structure This is where the idea becomes real. The group should create a legal entity such as: A nonprofit, a community land trust, a cooperative corporation, or a community development organization. This part matters because money, land, and housing need protection. The organization should have: Clear bylaws, a board of directors, voting rules, conflict-of-interest rules, financial transparency, and a written mission. This protects the community from confusion, corruption, and personal greed. The goal is not for one person to control everything. The goal is community stewardship. Step 4: Start a Community Housing Fund Once the structure is created, the group needs capital. Start simple. Imagine 100 families contributing $50 per month. That equals: $5,000 per month$60,000 per year Now imagine 500 families contributing $50 per month. That equals: $25,000 per month$300,000 per year This money can be used for down payments, legal fees, land surveys, property inspections, permits, repairs, and matching funds for grants. This is where Black economic circulation becomes real. Instead of money leaving the community every month, a portion of it is redirected into land ownership. Step 5: Find the First Property Do not start too big. Start with one property. The first project could be: A vacant lot, an abandoned home, a small duplex, a church-owned parcel, a tax sale property, or a small apartment building. The first property should be realistic. Do not try to build a 100-unit apartment complex on day one. Start with something the group can actually finish. The first successful project becomes proof. Proof attracts investors.Proof attracts grants.Proof attracts volunteers.Proof builds trust. Step 6: Build Partnerships Community housing cannot be built by emotion alone. It needs partnerships. The group should connect with: Local banks, Black-owned banks, credit unions, city housing departments, county officials, builders, architects, churches, nonprofits, grant writers, and real estate attorneys. The goal is to combine community money with outside funding. Community money shows seriousness. Outside funding helps scale the mission. A strong housing group can apply for grants, request donated land, use low-interest loans, and partner with local developers while still keeping community control. Step 7: Use Skilled Labor From the Community This is where housing becomes more than housing. It becomes job training. The project can include: Young people learning construction, retired tradesmen mentoring youth, local contractors getting paid, Black-owned businesses supplying materials, and families helping improve their own neighborhoods. Now the housing project creates: Jobs, skills, ownership, pride, safety, and future entrepreneurs. A house is not just a house when the community builds it. It becomes a training ground. Step 8: Set Rules That Protect Affordability This is critical. If the community builds housing but does not protect it, investors can eventually take it. Rules must be created to prevent speculation. For example: Homes cannot be flipped for massive profit.Rent increases must be limited.Priority may be given to local families.The land cannot be sold without community approval.Board members cannot secretly profit from deals.Financial reports must be shared regularly. This is how the mission stays clean. The goal is not quick money. The goal is permanent ownership. Step 9: House the First Family This is the moment everything becomes real. One renovated home.One family moved in.One block improved.One example created. That first family becomes the testimony. The community can show: This is what we built.This is what we own.This is what

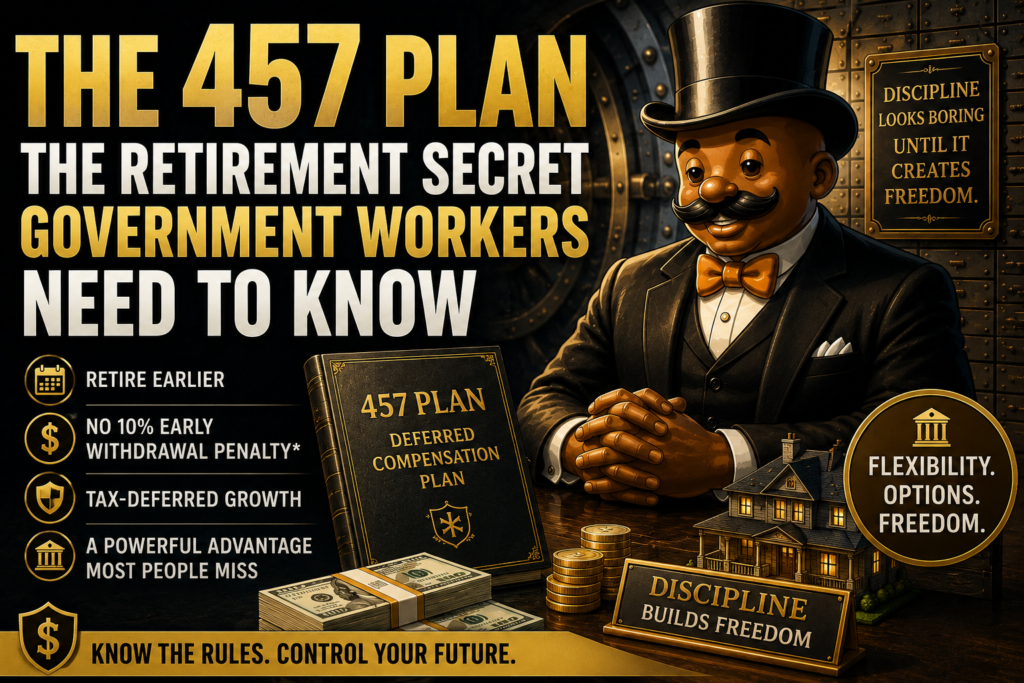

The 457 Plan: The Retirement Secret Government Workers Need to Know

Most people spend decades working toward retirement, only to discover that accessing their own money comes with restrictions, penalties, and limitations. But what if there was a retirement account that allowed certain workers to access their savings earlier than most Americans without the dreaded 10% early withdrawal penalty? For many government employees, that tool already exists. It’s called the 457 Deferred Compensation Plan. And it may be one of the most overlooked wealth-building tools in America. The Problem Most Workers Face Imagine spending 30 years saving money. You contribute faithfully to your retirement account. You sacrifice vacations. You skip luxuries. You invest consistently. Then one day, you decide you’re ready to leave your job. Maybe you want to start a business. Maybe you want to spend more time with family. Maybe you’re simply burned out. Then you discover that touching your retirement savings before age 59½ could trigger a 10% penalty on top of ordinary income taxes. Many Americans don’t realize this until it’s too late. The system encourages people to save, but often punishes them for wanting flexibility. This is where the 457 plan stands apart. What Is a 457 Deferred Compensation Plan? A 457 plan is a retirement savings account offered primarily to state and local government employees. This includes: Like a traditional 401(k), contributions are made before taxes. That means the money comes directly from your paycheck before Uncle Sam takes his share. Your investments grow tax-deferred until withdrawal. On the surface, it sounds very similar to a 401(k). But beneath the surface lies a major difference. The Hidden Advantage Let’s compare two workers. Worker #1 has a 401(k). Worker #2 has a 457 plan. Both are 52 years old. Both decide to leave their jobs. The 401(k) owner generally faces a 10% early withdrawal penalty if they access their retirement funds before age 59½. The 457 owner does not. Once they separate from their employer, they can generally withdraw funds without the additional penalty. Think about how powerful that is. This means the 457 isn’t simply a retirement account. It’s a flexibility account. It gives workers options. And options create freedom. Why Freedom Matters More Than Money Many people chase higher incomes their entire lives. But wealth isn’t just about money. Wealth is about control. Control over your schedule. Control over your opportunities. Control over how you spend your time. The ability to walk away from a job you no longer enjoy. The ability to pursue a business idea. The ability to care for loved ones when they need you. The ability to design your life instead of simply surviving it. That’s what makes the 457 so powerful. It gives people another path toward financial independence. Government Workers Have an Advantage Many government employees possess something that millions of Americans wish they had. Multiple retirement systems. A typical government worker may have: When used together, these tools can create a powerful financial foundation. The pension provides predictable income. The 457 provides flexibility. Additional investments create growth. The result is a retirement strategy that can provide both security and freedom. Not All 457 Plans Are Equal This is an important detail. There are two primary types of 457 plans: Governmental 457 Plans These are generally considered the safest option. Assets are held in trust for participants and remain protected. Non-Governmental 457 Plans These plans are commonly offered by certain nonprofit organizations. The assets may remain tied to the employer, creating additional risk. This is why every participant should ask: “Is my plan a governmental 457 plan?” That simple question could protect years of savings. The Power of Consistency Many people search for shortcuts. But wealth rarely comes from shortcuts. It usually comes from systems. Imagine contributing just a portion of every paycheck over decades. Those contributions grow. The growth compounds. The compounding creates momentum. Eventually, the account begins working harder than you do. That’s the real power behind retirement accounts. Not excitement. Not speculation. Not chasing trends. Consistency. As Sir Wealthington often says: Discipline looks boring until it creates freedom. Lessons for Everyone Even if you don’t have access to a 457 plan, there is still an important lesson here. The wealthy learn the rules. Most people simply work. Understanding financial systems often matters more than earning a higher income. The people who build lasting wealth usually know: Knowledge creates options. Options create freedom. Freedom creates wealth. Final Thoughts The 457 Deferred Compensation Plan isn’t flashy. It won’t go viral on social media. It won’t make headlines. But for millions of government workers, it may be one of the most valuable financial tools available. If you have access to one, learn the rules. Understand the benefits. Know the differences. And use it strategically. Because the goal isn’t simply retirement. The goal is having the freedom to choose your next chapter on your own terms. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. Build Your Family Bank Get The Family Bank Starter System:https://stan.store/blackdollarandculture/p/the-family-bank-starter-system Protect Generational Wealth Get Your Family Wealth Trust Blueprint Now – ILIT:https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now Hashtags 457 Plan Government Employees Retirement Planning Financial Freedom Wealth Building Personal Finance Early Retirement Family Bank Financial Literacy Investing Tax Strategy Pension Wealth Ownership Legacy Building Black Dollar And Culture Focus Keyphrase 457 Deferred Compensation Plan Slug 457-deferred-compensation-plan-explained Meta Description Learn how a 457 Deferred Compensation Plan works, why government workers have a unique retirement advantage, and how this powerful account can help create financial freedom and early retirement flexibility.

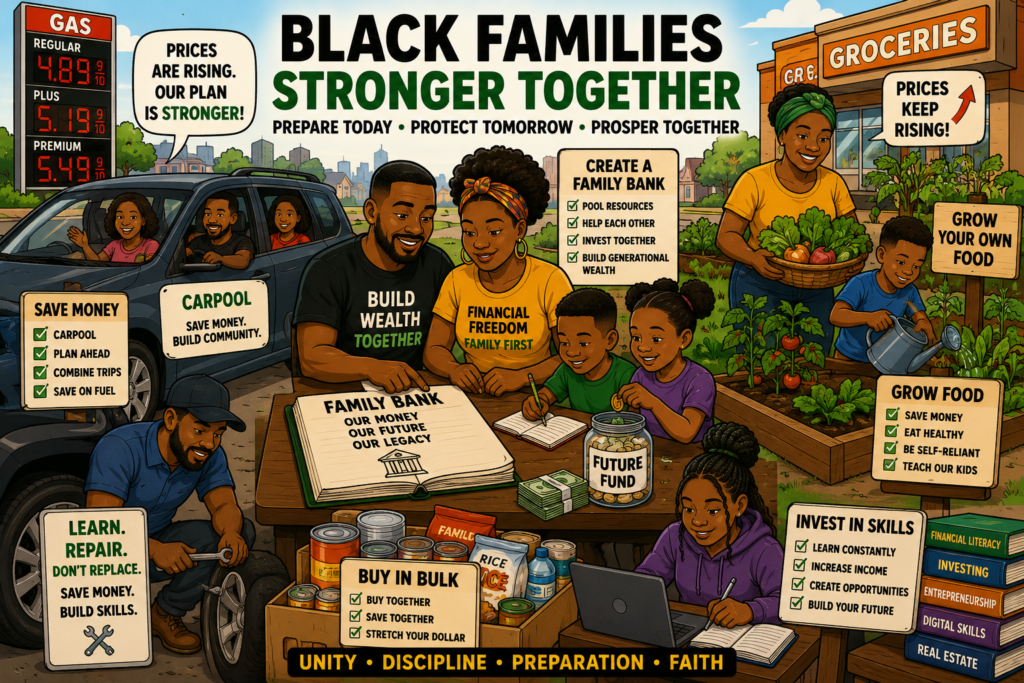

War, Inflation, and Survival: What Families Must Do Before Prices Rise Again

A war can begin thousands of miles away, but its effects often show up right in your neighborhood. Higher gas prices. More expensive groceries. Rising utility bills. Empty shelves. Economic uncertainty. Every time global conflict erupts, ordinary families end up paying the price. Not on the battlefield—but at the gas pump, in the grocery aisle, and through higher living costs. The families that survive economic storms aren’t always the richest. They’re often the most prepared. The question isn’t whether prices will rise again. History shows they will. The real question is: What are you doing today to protect your family tomorrow? Build A Family Emergency Fund Every family should have a financial cushion for unexpected events. Aim to save three to six months of essential expenses. This fund can help cover emergencies without relying on high-interest debt or credit cards. Economic uncertainty becomes easier to navigate when cash reserves are available. A family with savings has options. A family without savings has stress. Lesson: Cash creates options when times get tough. Create A Family Bank Strong families don’t just earn money—they organize it. A Family Bank allows relatives to pool resources, support one another during emergencies, fund business opportunities, and build wealth across generations. Instead of every household struggling alone, families can work together toward shared financial goals. The wealthy have used family financial systems for generations. There is no reason everyday families cannot do the same. Lesson: Unity creates economic strength. Reduce High-Interest Debt Inflation makes everything more expensive, including debt. Every dollar going toward credit card interest is a dollar that cannot be invested into your family’s future. Focus on eliminating high-interest balances and redirect those savings toward emergency funds, assets, and investments. Lesson: Debt limits flexibility during uncertain times. Grow Your Own Food You don’t need acres of land to begin producing food. A backyard, patio, balcony, or community garden can provide fresh vegetables and herbs while reducing grocery expenses. Consider growing: Many previous generations maintained gardens because they understood a simple truth: producing even a portion of your own food increases independence. Every tomato grown is one less tomato purchased. Lesson: Food security is financial security. Buy Essential Items Before Prices Rise When inflation accelerates, necessities often become more expensive. Gradually stock essentials such as: The goal isn’t panic buying. The goal is preparation. Lesson: Prepared families are less vulnerable to sudden price shocks. Carpool And Share Transportation Costs Fuel prices are often among the first expenses affected by global instability. Families, coworkers, church members, and neighbors can reduce costs through: Money saved on transportation can be redirected into savings, investments, or your Family Bank. Lesson: Cooperation lowers costs. Buy In Bulk As A Family One household has limited buying power. Several family members working together can purchase larger quantities of food and household essentials at lower prices. Bulk purchasing also creates a buffer against future shortages and inflation. This is group economics in action. Lesson: Group economics works. Learn To Repair Instead Of Replace When prices rise, replacing everything becomes expensive. Learning basic skills can save thousands over time: Every repair is money that stays in your family’s pocket. Lesson: Skills are assets. Invest In Skills That Produce Income Economic conditions may change, but valuable skills remain valuable. Consider learning: Skills create opportunities that inflation cannot easily destroy. Lesson: Your greatest asset is your ability to produce value. Diversify Your Income Depending on one paycheck can be risky during uncertain times. Look for additional income streams through: Multiple streams of income provide stability when one source is disrupted. Lesson: Wealthy families rarely rely on a single source of income. Buy Assets, Not Just Stuff Many people spend money on liabilities while neglecting assets. Consider acquiring assets that can generate income or appreciate over time: Assets help families fight inflation rather than merely survive it. Lesson: Assets create financial resilience. Protect Wealth With Proper Planning Building wealth is important. Keeping it is even more important. Many families lose assets through probate, taxes, poor planning, and lack of financial structure. Tools such as trusts and life insurance can help protect what you’ve built for future generations. Final Thoughts As prices rise and uncertainty grows, the answer isn’t panic. The answer is preparation. Build a Family Bank. Grow food. Reduce debt. Carpool. Buy in bulk. Learn useful skills. Create multiple streams of income. Strengthen family relationships. The families that thrive during difficult times are often the ones that depend less on outside systems and more on each other. While others complain about rising prices, your family can be building a foundation strong enough to weather any economic storm. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. FAQ Will war always cause inflation? Not always, but wars often disrupt energy supplies, transportation, trade routes, and production, which can contribute to higher prices. How much emergency savings should I have? Most financial experts recommend three to six months of essential living expenses. Can I start a Family Bank with very little money? Yes. The habit and structure matter more than the starting amount. Many successful family systems begin with small weekly contributions. What is the easiest food to grow for beginners? Tomatoes, peppers, herbs, lettuce, and collard greens are popular beginner-friendly options. Hashtags #BlackDollarAndCulture #FamilyBank #Inflation #EconomicPreparedness #GenerationalWealth #FinancialLiteracy #GroupEconomics #BlackWealth #WealthBuilding #EmergencyFund #FoodSecurity #FinancialFreedom #AssetBuilding #CommunityEconomics #FamilyLegacy Focus Keyphrase War and Rising Prices Slug war-inflation-and-survival-family-preparation-guide Meta Description Learn how to protect your family from rising prices, inflation, and economic uncertainty through Family Banks, emergency savings, gardening, bulk buying, carpooling, asset ownership, and wealth-building strategies.

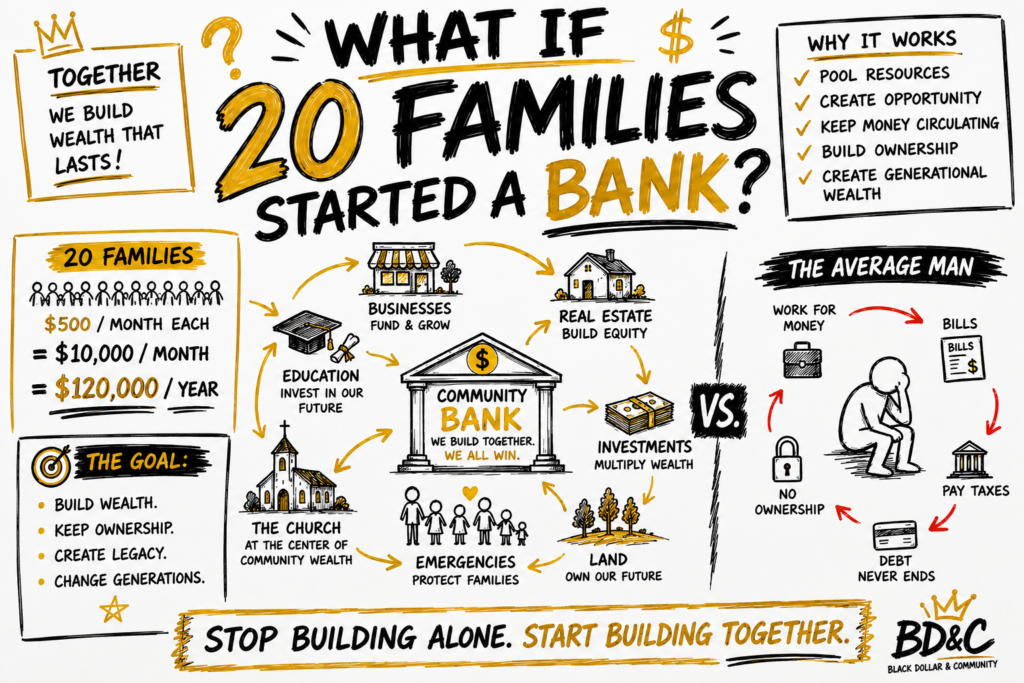

What If 20 Families Started a Bank? The Community Wealth Blueprint That Could Change Everything

Most families are taught to survive individually. Work harder.Save what you can.Handle emergencies alone.Take on debt when life gets difficult. But wealthy communities have often understood something different: Group economics multiplies power. So what would happen if twenty families stopped building separately… and started building together? Not a literal licensed bank. But a structured community wealth system designed around ownership, circulation, discipline, and long-term legacy. Think about it. If twenty families contributed just $500 per month into a structured economic system, that would create: Now imagine what that capital could potentially support: Suddenly, families are no longer depending entirely on outside institutions for every opportunity. That changes the mindset completely. Why Group Economics Matters One of the biggest problems in struggling communities is not always the absence of money. It is often the absence of systems. Money enters the community…and immediately leaves the community. No circulation.No ownership.No infrastructure.No long-term strategy. That is why concepts like: have historically been so powerful. Black Wall Street understood this. Mutual aid societies understood this. Church communities once understood this deeply. The goal was never simply making money. The goal was creating systems capable of sustaining future generations. This is exactly why the Family Bank concept matters. A Family Bank is not a physical bank building. It is a structured system where families organize money intentionally instead of emotionally. The Family Bank teaches: Instead of constantly financing everything through outside lenders, families begin creating internal systems of support and capital. That mindset shift is powerful. 📘 Build Your Own Family Wealth Structure Here:The Family Bank Starter System Why Structure Matters Now let’s be clear. Any community wealth system requires: Without structure, money becomes chaos. That is why wealthy institutions operate through systems and policies. Not emotions. The same principle applies to families and communities. The ILIT and Legacy Protection Building wealth is one thing. Protecting wealth is another. That’s why wealthy families often use trusts and structured estate planning strategies to help preserve assets across generations. One powerful concept is the ILIT:Irrevocable Life Insurance Trust. An ILIT can help structure how life insurance wealth is transferred, protected, and distributed to heirs. Because many families receive money with no instructions, no protections, and no long-term strategy. That is one reason wealth disappears quickly. 🏦 Learn More About ILIT Wealth Protection Here:Get Your Family Wealth Trust Blueprint Now – ILIT The Bigger Question What would happen if families stopped building alone? What would happen if communities focused on: instead of only survival? That question could change entire communities. Because the goal is not just making money. The goal is building systems strong enough to outlive us. #GroupEconomics #FamilyBank #BlackDollarAndCulture #GenerationalWealth #CommunityWealth #BlackWallStreet #CooperativeEconomics #Ownership #EconomicPower #ILIT #WealthBuilding #FamilyLegacy #BuildTogether #CommunityBank #FinancialFreedom Focus Keyphrase: What If 20 Families Started a BankSlug: what-if-20-families-started-a-bankMeta Description: Discover how 20 families pooling resources could create a powerful community wealth system through group economics, ownership, Family Banking, and ILIT wealth protection strategies.

If You Don’t Control the Flow of Money… You Don’t Control Your Future (PowerNomics)

There are moments in history when the answers are already written… but ignored. In 1995, Dr. Claud Anderson released PowerNomics — not as motivation, not as theory, but as a blueprint. A structured plan to build economic power through one principle most people still overlook: group economics. And decades later, the question isn’t whether it works… it’s whether we’re finally ready to apply it. Because the issue was never a lack of talent, creativity, or ambition. The issue has always been structure. Money flows in… and flows right back out. Paychecks are earned, spent, and gone before they ever have the chance to circulate, multiply, or build anything lasting. That’s not an economy — that’s a pass-through system. And as long as money behaves that way, wealth will never take root. Group economics starts with a simple but uncomfortable truth: you cannot build wealth alone in a system designed around collective power. Every successful community understands this. Their money doesn’t just move — it moves with intention. It circulates internally. It supports businesses within the group. It hires within the group. It builds systems that reinforce itself before reaching outward. That’s not accidental. That’s design. When Dr. Claud Anderson laid out this framework, he wasn’t asking for support out of sympathy — he was outlining a strategy of survival and control. Because whoever controls the flow of money… controls the outcome. And when money leaves immediately, so does opportunity, ownership, and influence. Think about it in real terms. A dollar earned today can either disappear by tomorrow… or circulate five, six, seven times — creating jobs, sustaining businesses, and funding growth along the way. That’s the difference between spending and building. One is temporary. The other is intentional. But group economics requires a shift in thinking — from individual success to collective progress. It means asking different questions before every transaction: Who am I supporting? Where is this money going? What is this building? Because every dollar is a vote. And too often, those votes are cast without strategy. The blueprint is clear. First, money must circulate. Then, ownership must follow. Then institutions are built. And finally, legacy is secured. But without that first step — without group economics — everything else collapses before it ever begins. This is why so many efforts fail. People jump straight to ownership without circulation. They try to build institutions without a base. They aim for wealth without a system to sustain it. And when the foundation isn’t there, nothing holds. That’s what makes this conversation different. This isn’t about doing more. It’s about doing differently. Because once money begins to circulate, something powerful happens. Businesses stabilize. Networks form. Opportunities increase. And slowly, control begins to shift. Not overnight — but consistently. That’s how real economic power is built: quietly, strategically, and collectively. And that’s exactly why this message still matters today. Because the blueprint was never lost. It was just never fully applied. So the real question isn’t whether group economics works… It’s whether we’re finally ready to stop letting money pass through our hands — and start making it work for us. Start Building the System (Don’t Just Learn It) If this message resonates, the next step is structure — not just understanding. 👉 Build Your Internal Economy (Family Bank Starter System)https://stan.store/blackdollarandculture/p/the-family-bank-starter-system 👉 Protect & Pass Down Wealth (ILIT Trust Blueprint)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now Because building wealth is one thing… Keeping it — and passing it down — is everything. 🔁 Support the Movement 👉 Discover and support businesses that keep money circulating:https://blkcirculation.com 📊 FAQ: Group Economics & PowerNomics What is group economics?It’s the practice of circulating money within a community to build collective wealth, reduce dependency, and increase economic control. Why is group economics important?Because money that leaves immediately cannot multiply. Circulation is what turns income into wealth. What did Dr. Claud Anderson teach in PowerNomics?That economic power comes from structure — group economics, ownership, institutions, and long-term planning. Why hasn’t this been widely applied?Because most systems condition individuals to operate independently rather than collectively, weakening economic impact. 🔑 Final Thought They knew this in 1995. The blueprint didn’t change. The system didn’t change. The only thing left… is whether we will. #GroupEconomics #PowerNomics #ClaudAnderson #BlackWealth #GenerationalWealth #EconomicEmpowerment #Ownership #WealthBuilding #FinancialLiteracy #BlackBusiness #CommunityWealth #MoneyCirculation #FamilyBank #ILIT #WealthStrategy Group Economics PowerNomics group-economics-powernomics-1995-blueprint Discover Dr. Claud Anderson’s Group Economics blueprint from PowerNomics and learn how to build, circulate, and protect generational wealth today.

Ella Baker: The Architect of Grassroots Power They Rarely Teach

History remembers the speeches. But historians remember the structure. And when you study the Civil Rights Movement closely, one name keeps appearing—not in headlines, but in the foundation: Ella Baker. She was not simply a participant in history. She was one of its chief designers. Early Life: A Mind Formed by Resistance Ella Baker was born in Norfolk, Virginia, and raised in North Carolina in the early 1900s—a time when Black life in America was defined by segregation, violence, and systemic exclusion. But her worldview wasn’t shaped by fear. It was shaped by story and resistance. Her grandmother, who had been enslaved, told her stories of refusing to marry a man chosen by a slave owner—choosing punishment over submission. That story stayed with Baker. It taught her something critical early: 👉 Authority is not always legitimate👉 Resistance is a choice She carried that mindset into everything she built. Education and Awakening Baker attended Shaw University, one of the oldest HBCUs in the country, where she graduated as valedictorian. But unlike many who pursued personal advancement, Baker moved toward collective struggle. In the 1930s, during the Great Depression, she became involved in cooperative economic movements—organizations focused on shared ownership and group survival. This is often overlooked. Before civil rights organizing…Ella Baker was already studying economic systems. The NAACP Years: Building From the Ground Up When Baker joined the NAACP, she didn’t stay in an office. She traveled. Town to town.Community to community. Listening. Organizing. Building. She eventually became a national director of branches, helping grow the NAACP’s reach across the country. But more importantly… She built local leadership. Not followers. Leaders. That distinction would define her entire legacy. Challenging Power Within the Movement Baker later worked with the Southern Christian Leadership Conference, where she crossed paths with Martin Luther King Jr.. But she didn’t blindly follow. In fact, she challenged the structure of the organization. She believed it was too dependent on charismatic leadership. Too centralized. Too fragile. Her position was clear: A movement that depends on one leader… can collapse with one leader She pushed for a broader base of empowered individuals. That idea would soon reshape the movement. The Birth of SNCC: Her Most Powerful Contribution In 1960, as student sit-ins spread across the South, Baker saw something others didn’t: A new generation ready to lead. She organized a meeting at Shaw University, bringing these young activists together. From that meeting came the Student Nonviolent Coordinating Committee. SNCC became one of the most effective grassroots organizations in American history. And its structure reflected Baker’s philosophy: This wasn’t just activism. This was strategy. A Leadership Style Rooted in Humility Unlike many public figures, Ella Baker avoided the spotlight. She didn’t seek recognition. She didn’t build a personal brand. She built people. She mentored young leaders like: And through them, her influence multiplied. This is why her impact is so difficult to measure. It lives inside the actions of others. The Historian’s Conclusion: Why She Matters From a historical standpoint, Ella Baker represents a different model of power. Not symbolic power. Not performative power. Structural power. The kind that: She understood something timeless: If you want change to last… you must design it to survive you BD&C Perspective: This Is the Same Blueprint for Wealth Take her philosophy and apply it today: Most people chase income. Few build systems. Most people build for themselves. Few build for generations. Ella Baker’s model translates directly into modern wealth strategy: This isn’t new thinking. It’s historical thinking. Build What Lasts If you’re serious about applying this level of strategy to your life: 👉 Start your family’s internal systemThe Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 👉 Lock in long-term protection and legacyGet Your Family Wealth Trust Blueprint (ILIT)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now Final Reflection Ella Baker didn’t need a microphone to shape history. She needed vision. Discipline. And a deep understanding of how power really works. Her name may not always be the loudest… But her impact is among the deepest. FAQ: Ella Baker in Depth Where was Ella Baker born?She was born in Norfolk, Virginia, and raised in North Carolina. What made her leadership unique?She focused on grassroots organizing and empowering everyday people instead of relying on centralized leadership. Who did she mentor?She influenced major figures like John Lewis and Diane Nash, among many others. Why is she less well-known?Because she intentionally stayed behind the scenes, prioritizing impact over recognition. Continue the Real Story 📘 The First World Before Erasurehttps://stan.store/blackdollarandculture/p/the-first-world-before-erasure Final Word Some leaders build movements. Ella Baker built the people who built the movements. That difference… Changes everything. #EllaBaker #BlackHistory #CivilRightsMovement #SNCC #NAACP #BlackLeaders #GenerationalWealth #BlackDollar #EconomicPower #Ownership #Legacy #BDandC Focus Keyphrase: Ella Baker civil rights strategistSlug: ella-baker-civil-rights-strategistMeta Description: Explore the life of Ella Baker, the strategist behind the Civil Rights Movement, and learn how her approach to leadership connects to generational wealth and lasting systems today.

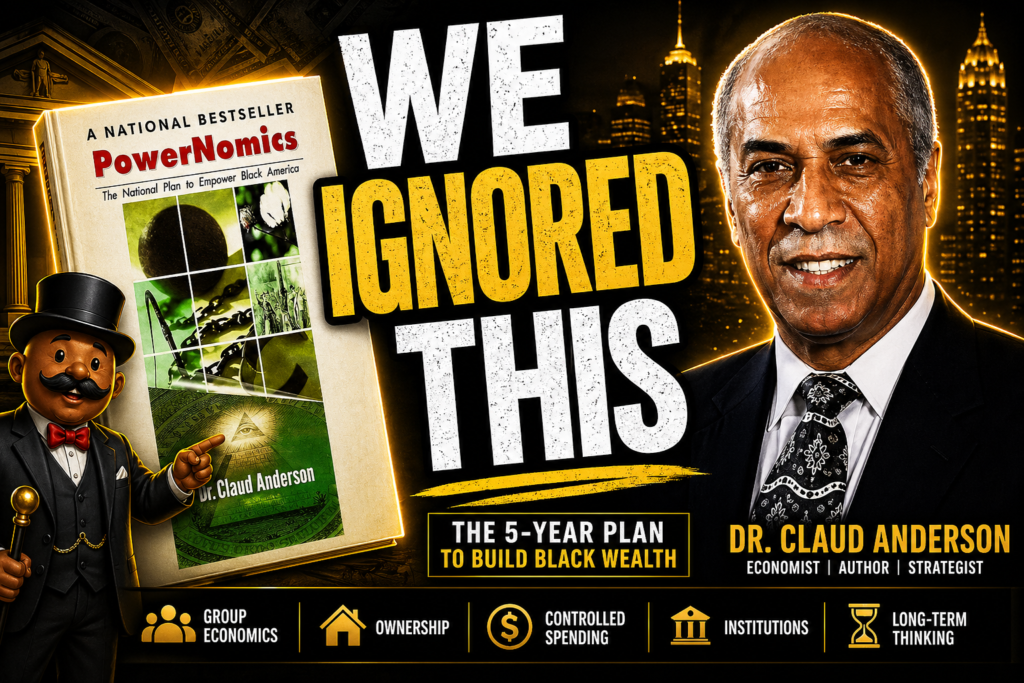

PowerNomics Explained: The 1995 Blueprint for Black Wealth We Still Haven’t Used

In 1995, a blueprint was laid out that most people never truly studied. Not because it was hidden.Not because it was complicated. But because it required something most people weren’t ready for: Discipline, structure, and long-term thinking. Dr. Claude Anderson didn’t speak in vague ideas. He didn’t deal in motivation. He laid out a system — one that explained exactly why wealth wasn’t sticking, and what it would take to change that. And if we’re being honest… The problem was never a lack of information. It was a lack of application. The Real Issue Was Never Just Money Most people think the problem is income. “If we just made more, everything would change.” But that’s not how wealth works. Dr. Anderson pointed to something deeper — something most people overlook: Control. You can make money and still be broke in the long run if you don’t control: If money comes in and immediately leaves, it doesn’t matter how much you earn. You’re not building wealth. You’re financing someone else’s. How Money Actually Builds Power Let’s slow this down and make it real. Imagine two different communities. Community A The money is gone within days. No ownership. No return. No growth. Community B Now that same dollar: It doesn’t just move. It multiplies. That’s the difference between spending and circulation. And that difference determines everything. Why Ownership Is the Foundation One of the clearest messages from PowerNomics is this: If you don’t own it, you don’t control it. That applies to: When you don’t own these, you are always operating inside someone else’s system. That means: You participate… but you don’t direct. And participation without ownership doesn’t build lasting wealth. The Hidden Trap: High Income, No Structure This is where a lot of people today get caught. There are more people making money now than ever before. But ask yourself: Because here’s the reality: You can have a high income and still leave nothing behind. Why? Because income without structure turns into: But not long-term power. Why Wealth Keeps Resetting Every Generation This is one of the most important parts of the conversation. A generation works hard. They buy a house.They save some money.They build something. Then life happens: And because there’s no structure: So the next generation… Starts over. That’s not bad luck. That’s a missing system. The Part PowerNomics Tried to Fix Dr. Anderson wasn’t just pointing out problems. He was trying to install a mindset shift: From: To: From: To: From: To: Because wealth isn’t about one person getting ahead. It’s about building something that continues after you’re gone. What This Looks Like in Real Life Let’s bring this down to something practical. Instead of thinking:“I made money this year.” The question becomes:“What system did I build this year?” That could mean: Because once systems are in place… Money starts working differently. This Is Where Most People Need to Get Serious A lot of people agree with these ideas. But agreement doesn’t change anything. Execution does. And execution requires: Because the default system is designed for money to leave your hands. You have to intentionally build something that keeps it. If You’re Ready to Move From Ideas to Structure This is where most people stop. They understand the concept… but don’t build the system. If you’re serious about applying what you just read, you need tools that actually help you implement it. 👉 Start building your internal system here:The Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 👉 Make sure what you build actually lasts:Get Your Family Wealth Trust Blueprint (ILIT)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now 👉 Understand the deeper historical context behind all of this:The First World Before Erasurehttps://stan.store/blackdollarandculture/p/the-first-world-before-erasure The Truth Most People Don’t Want to Say Out Loud The blueprint wasn’t missing. It wasn’t hidden. It was there. Since 1995. Clear. Direct. Actionable. So the real question now isn’t about awareness. It’s about accountability. What are you going to build with the information you already have? FAQ What is PowerNomics?A framework created by Dr. Claude Anderson focused on building wealth through ownership, group economics, and strategic control of resources. Why is ownership more important than income?Because ownership gives you control over assets, opportunities, and long-term wealth, while income alone is temporary. What is a Family Bank?A structured system where families pool and circulate money internally to fund opportunities and build wealth collectively. What is an ILIT and why does it matter?An Irrevocable Life Insurance Trust helps protect and transfer wealth efficiently, preventing assets from being lost through taxes or poor planning. #PowerNomics #BlackWealth #GroupEconomics #OwnershipMatters #GenerationalWealth #FamilyBank #FinancialStrategy #WealthBuilding #EconomicPower #BlackDollar Focus Keyphrase: PowerNomics Blueprint ExplainedSlug: powernomics-blueprint-explainedMeta Description: A deep breakdown of Dr. Claude Anderson’s PowerNomics blueprint and how ownership, circulation, and structure build real generational wealth.