How One Rental Property Can Change Your Family’s Financial Future Forever

Introduction Many people believe they need dozens of properties, millions of dollars, or years of experience before real estate can make a meaningful impact on their finances. The truth is that for many families, wealth begins with a single property. One rental property may not make you rich overnight, but it can start a financial chain reaction that changes the trajectory of your family for decades. It can create monthly cash flow, build equity, provide tax advantages, and eventually become an asset that can be passed down to future generations. The journey to wealth often starts with one door. The Difference Between Income and Ownership Most families rely almost entirely on earned income. They work.They get paid.They spend.Then the cycle repeats. While employment can provide stability, ownership creates leverage. When you own a rental property, someone else helps pay for an asset that you control. Every rent payment contributes to your wealth-building journey. Instead of relying solely on your paycheck, you now have an asset working alongside you. Rental Income Creates Additional Cash Flow One of the biggest benefits of rental property ownership is monthly cash flow. Imagine owning a property that generates income every month after expenses are paid. That extra income can be used to: Over time, even a few hundred dollars per month can add up to thousands of dollars annually. The goal is not simply earning more money. The goal is creating income streams that do not depend entirely on your labor. Equity Builds Wealth Quietly Every mortgage payment typically contains a principal portion. That means every month you own the property, a portion of the debt is reduced. At the same time, the property’s value may increase over the long term. This creates equity. Equity is one of the most powerful wealth-building tools available because it grows quietly in the background while life continues. Many families underestimate how valuable this can become after 10, 20, or 30 years. Appreciation Can Multiply Your Wealth Historically, real estate has appreciated over long periods of time. While markets move up and down, many property owners benefit from increasing property values over decades. For example: A $200,000 property that grows in value over time may eventually be worth significantly more than its original purchase price. Combined with rental income and loan paydown, appreciation can create a powerful wealth-building formula. One Property Can Lead to Another Many successful investors did not start with ten properties. They started with one. The cash flow and equity from the first property often help fund future opportunities. Property #1 can help purchase Property #2. Property #2 can help purchase Property #3. The process may take years, but wealth often grows through patience and consistency rather than speed. Creating Generational Wealth Perhaps the greatest benefit of rental property ownership is the ability to transfer assets to future generations. Many families inherit bills. Wealthy families often inherit assets. A rental property can provide: When structured properly, a rental property can continue benefiting children, grandchildren, and future generations. Why Ownership Matters The wealthiest families in history have consistently focused on ownership. They own businesses. They own land. They own real estate. Ownership creates opportunities that employment alone often cannot. A rental property may not seem life-changing today, but decades from now it could become one of the most important financial decisions your family ever makes. Final Thoughts One rental property will not solve every financial problem. However, it can create a powerful foundation for long-term wealth. It can generate cash flow, build equity, provide appreciation, and create opportunities for future generations. Many families spend years waiting for the perfect opportunity. The families who build wealth often start with what they can afford and allow time to do the heavy lifting. Sometimes changing your family’s future begins with a single property. Build Your Family Wealth System If you’re serious about protecting your family and building long-term wealth, start here: 🏠 Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 🛡️ Family Wealth Trust (ILIT Blueprint)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now Focus Keyphrase One Rental Property Can Change Your Family’s Financial Future Tags Rental Property, Real Estate Investing, Passive Income, Cash Flow, Generational Wealth, Family Wealth, Financial Freedom, Real Estate, Family Bank, Black Dollar and Culture, Wealth Building, Property Ownership, Rental Income, Investing, Ownership Economics Meta Description Discover how a single rental property can create cash flow, build equity, generate passive income, and help your family create generational wealth. Focus Keyphrase One Rental Property Can Change Your Family’s Financial Future URL Slug one-rental-property-can-change-your-familys-financial-future

There Is No Recession on Productive Land

Every election season, people are promised prosperity. Every economic downturn brings fear. Every market correction sends investors scrambling for answers. Yet through every recession, depression, inflation crisis, and political transition, one asset has quietly continued creating wealth: Land. Not stocks. Not social media followers. Not government programs. Land. For thousands of years, the wealthiest families on Earth have understood a simple truth: If you control productive land, you control opportunity. While many people spend their lives chasing the next trend, landowners spend their lives building assets that continue producing regardless of who occupies the White House, what the stock market is doing, or what the latest headlines say. The power isn’t in politics. The power is in the land. Productive Land Doesn’t Watch the News Think about it. A fruit tree doesn’t stop producing because the economy enters a recession. A chicken doesn’t stop laying eggs because inflation rises. A greenhouse doesn’t care who won the election. A productive piece of land continues doing what it has always done: producing value. This is why land ownership has remained one of the most reliable paths to wealth throughout human history. Markets rise. Markets fall. But productive assets continue producing. That’s the difference between speculation and ownership. Agriculture Is the Original Wealth Builder Long before Wall Street existed, agriculture created wealth. Long before banks were built, agriculture created wealth. Long before corporations existed, agriculture created wealth. Food remains one of the few products every human being on Earth must consume every single day. People can delay vacations. People can postpone buying a new car. People can cancel subscriptions. But people cannot stop eating. Food production is one of the oldest and most essential businesses in human history. That reality is unlikely to change. Artificial intelligence may transform industries. Technology may reshape the economy. But somebody will still need to grow food. The Difference Between Consumers and Producers Many people spend their entire lives consuming. Consuming products. Consuming entertainment. Consuming trends. Consuming debt. The wealthy often focus on something different: Production. Producers create value. Producers own assets. Producers generate income. Land transforms people from consumers into producers. A small garden produces food. An orchard produces fruit. A farm produces income. A greenhouse produces opportunity. Ownership changes everything. Why Communities Should Think About Land Again Many communities spend millions of dollars every year importing food, products, and services from outside their neighborhoods. Money enters. Money leaves. The cycle repeats. But what happens when communities begin producing more of what they consume? Money circulates longer. Businesses grow. Jobs are created. Families gain skills. Ownership increases. Economic resilience improves. Every garden, farm, greenhouse, and agricultural business represents one more step toward economic independence. You Don’t Need Hundreds of Acres One of the biggest misconceptions about agriculture is that you need a massive farm to begin. You don’t. Start where you are. Plant herbs. Plant vegetables. Learn gardening. Grow fruit trees. Support local farmers. Invest in agricultural education. Purchase a small piece of rural land when possible. The goal is not to become a large-scale farmer overnight. The goal is to develop productive assets over time. Small beginnings often create large outcomes. Land Creates Legacy Many people dream about leaving wealth behind. Few people think about the assets that create wealth. Imagine passing down: These assets can continue generating value long after the original owner is gone. That is the power of ownership. That is the power of productive land. That is the power of legacy. The Future Belongs to Owners The next generation will face new challenges. Artificial intelligence. Automation. Economic uncertainty. Global competition. But one thing is unlikely to change: People will still need food. People will still need housing. People will still need land. The families that understand this today may be building the foundation for wealth tomorrow. Not through chasing trends. Not through waiting on promises. But through ownership. Final Thoughts The headlines may tell you to panic. The politicians may tell you to wait. The markets may tell you to worry. But productive land tells a different story. Plant something. Grow something. Build something. Own something. Because there is no recession on productive land. There is only opportunity for those willing to cultivate it. Continue Building Your Family’s Legacy 📘 The Family Bank Starter KitLearn how families can create their own systems for saving, investing, and building generational wealth. 📘 ILIT: Infinite Banking & Legacy PlanningDiscover strategies used to protect wealth, create financial flexibility, and leave a lasting legacy for future generations. Visit BLKCirculation.com to learn more. SEO Title: There Is No Recession on Productive Land Focus Keyphrase: Productive Land Wealth Slug: there-is-no-recession-on-productive-land Meta Description: Discover why productive land remains one of the most powerful wealth-building assets regardless of economic conditions. Learn how land ownership, agriculture, and production can create lasting financial security and generational wealth. Black Dollar & CultureOwnership. Circulation. Legacy.

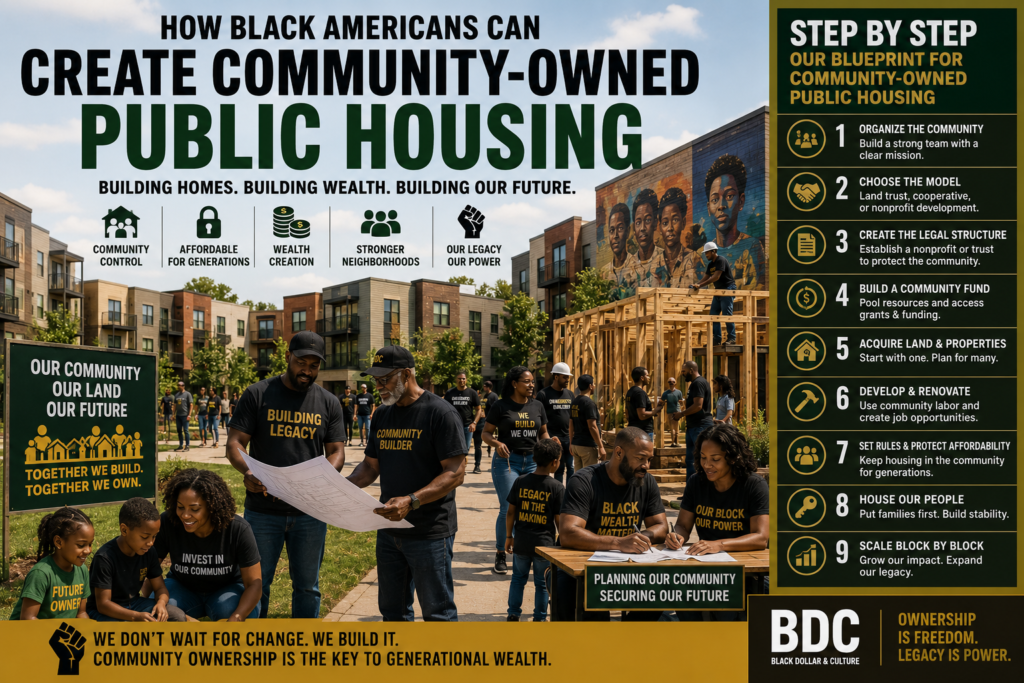

How Black Communities Can Build Public Housing Without Waiting on Government Housing

Housing has always been one of the biggest keys to power in America. Whoever controls the land controls the neighborhood. Whoever controls the neighborhood controls the businesses, schools, safety, rent prices, and future wealth of the people living there. For Black Americans, the housing conversation cannot only be about renting cheaper apartments or waiting for someone else to build affordable housing. We have to think bigger. The real question is: How can we create housing that the community owns, protects, and passes down? This is where community-owned housing comes in. Community-owned housing is when people come together to buy land, build homes, control affordability, and keep property from being taken over by outside investors. It is not just about shelter. It is about ownership, protection, legacy, and economic power. Step 1: Form a Housing Vision Group The first step is gathering the right people. This group should include: Community leaders, church leaders, real estate agents, contractors, electricians, plumbers, attorneys, accountants, business owners, investors, and serious families who care about ownership. This cannot be just a conversation group. It has to become an action group. The mission should be clear: Acquire land, build or renovate homes, and keep housing affordable for Black families and working-class families. Start with 5 to 10 serious people. Not everybody has to have money. Some people may bring skills. Some may bring land. Some may bring credit. Some may bring legal knowledge. Some may bring construction experience. The first goal is organization. Without organization, money gets wasted.Without leadership, ideas die.Without a structure, the community stays dependent. Step 2: Choose the Ownership Model Before buying property, the group must decide how the housing will be owned. There are three strong models. Community Land Trust A Community Land Trust is one of the strongest options. The community owns the land through a nonprofit trust. Families may rent or buy homes on that land, but the land itself stays protected. This keeps outside investors from buying up the neighborhood and raising prices. The land becomes a permanent community asset. Housing Cooperative A housing cooperative means the residents collectively own the property. Instead of paying rent to an outside landlord, residents own shares in the cooperative. They help make decisions, vote on leadership, and share responsibility. This works well for apartments, duplexes, townhomes, or small communities. Church or Nonprofit Housing Development Many Black churches and nonprofits already own land. Some of that land sits unused. That land could become senior housing, starter homes, rental units, tiny homes, duplexes, or family housing. Churches already have trust, leadership, and community connection. If structured correctly, church-owned land can become a powerful housing solution. Step 3: Create the Legal Structure This is where the idea becomes real. The group should create a legal entity such as: A nonprofit, a community land trust, a cooperative corporation, or a community development organization. This part matters because money, land, and housing need protection. The organization should have: Clear bylaws, a board of directors, voting rules, conflict-of-interest rules, financial transparency, and a written mission. This protects the community from confusion, corruption, and personal greed. The goal is not for one person to control everything. The goal is community stewardship. Step 4: Start a Community Housing Fund Once the structure is created, the group needs capital. Start simple. Imagine 100 families contributing $50 per month. That equals: $5,000 per month$60,000 per year Now imagine 500 families contributing $50 per month. That equals: $25,000 per month$300,000 per year This money can be used for down payments, legal fees, land surveys, property inspections, permits, repairs, and matching funds for grants. This is where Black economic circulation becomes real. Instead of money leaving the community every month, a portion of it is redirected into land ownership. Step 5: Find the First Property Do not start too big. Start with one property. The first project could be: A vacant lot, an abandoned home, a small duplex, a church-owned parcel, a tax sale property, or a small apartment building. The first property should be realistic. Do not try to build a 100-unit apartment complex on day one. Start with something the group can actually finish. The first successful project becomes proof. Proof attracts investors.Proof attracts grants.Proof attracts volunteers.Proof builds trust. Step 6: Build Partnerships Community housing cannot be built by emotion alone. It needs partnerships. The group should connect with: Local banks, Black-owned banks, credit unions, city housing departments, county officials, builders, architects, churches, nonprofits, grant writers, and real estate attorneys. The goal is to combine community money with outside funding. Community money shows seriousness. Outside funding helps scale the mission. A strong housing group can apply for grants, request donated land, use low-interest loans, and partner with local developers while still keeping community control. Step 7: Use Skilled Labor From the Community This is where housing becomes more than housing. It becomes job training. The project can include: Young people learning construction, retired tradesmen mentoring youth, local contractors getting paid, Black-owned businesses supplying materials, and families helping improve their own neighborhoods. Now the housing project creates: Jobs, skills, ownership, pride, safety, and future entrepreneurs. A house is not just a house when the community builds it. It becomes a training ground. Step 8: Set Rules That Protect Affordability This is critical. If the community builds housing but does not protect it, investors can eventually take it. Rules must be created to prevent speculation. For example: Homes cannot be flipped for massive profit.Rent increases must be limited.Priority may be given to local families.The land cannot be sold without community approval.Board members cannot secretly profit from deals.Financial reports must be shared regularly. This is how the mission stays clean. The goal is not quick money. The goal is permanent ownership. Step 9: House the First Family This is the moment everything becomes real. One renovated home.One family moved in.One block improved.One example created. That first family becomes the testimony. The community can show: This is what we built.This is what we own.This is what

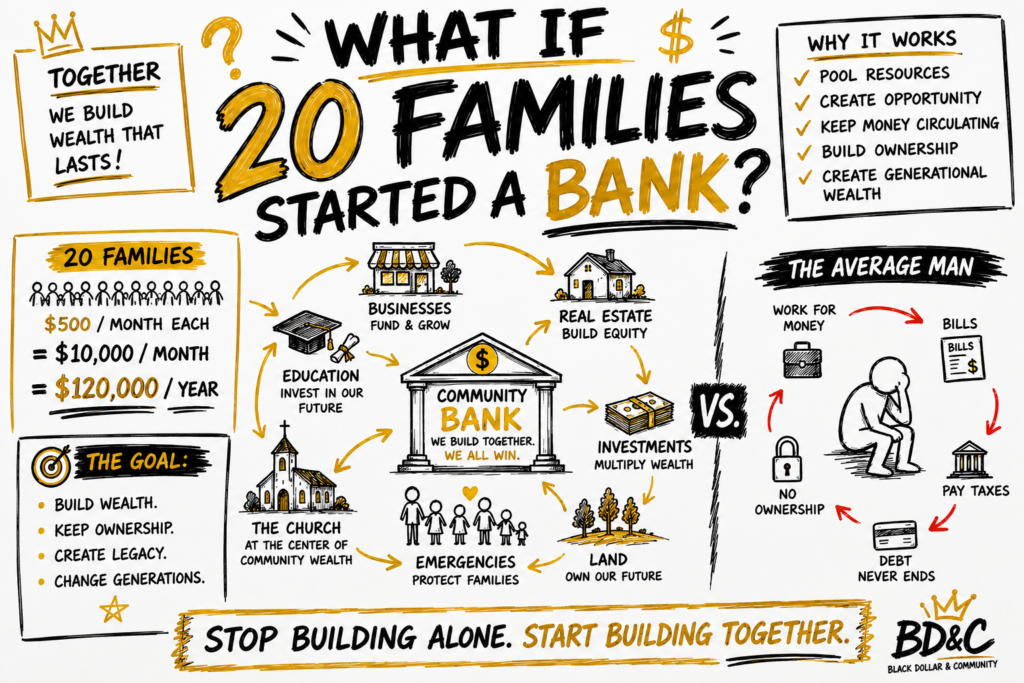

What If 20 Families Started a Bank? The Community Wealth Blueprint That Could Change Everything

Most families are taught to survive individually. Work harder.Save what you can.Handle emergencies alone.Take on debt when life gets difficult. But wealthy communities have often understood something different: Group economics multiplies power. So what would happen if twenty families stopped building separately… and started building together? Not a literal licensed bank. But a structured community wealth system designed around ownership, circulation, discipline, and long-term legacy. Think about it. If twenty families contributed just $500 per month into a structured economic system, that would create: Now imagine what that capital could potentially support: Suddenly, families are no longer depending entirely on outside institutions for every opportunity. That changes the mindset completely. Why Group Economics Matters One of the biggest problems in struggling communities is not always the absence of money. It is often the absence of systems. Money enters the community…and immediately leaves the community. No circulation.No ownership.No infrastructure.No long-term strategy. That is why concepts like: have historically been so powerful. Black Wall Street understood this. Mutual aid societies understood this. Church communities once understood this deeply. The goal was never simply making money. The goal was creating systems capable of sustaining future generations. This is exactly why the Family Bank concept matters. A Family Bank is not a physical bank building. It is a structured system where families organize money intentionally instead of emotionally. The Family Bank teaches: Instead of constantly financing everything through outside lenders, families begin creating internal systems of support and capital. That mindset shift is powerful. 📘 Build Your Own Family Wealth Structure Here:The Family Bank Starter System Why Structure Matters Now let’s be clear. Any community wealth system requires: Without structure, money becomes chaos. That is why wealthy institutions operate through systems and policies. Not emotions. The same principle applies to families and communities. The ILIT and Legacy Protection Building wealth is one thing. Protecting wealth is another. That’s why wealthy families often use trusts and structured estate planning strategies to help preserve assets across generations. One powerful concept is the ILIT:Irrevocable Life Insurance Trust. An ILIT can help structure how life insurance wealth is transferred, protected, and distributed to heirs. Because many families receive money with no instructions, no protections, and no long-term strategy. That is one reason wealth disappears quickly. 🏦 Learn More About ILIT Wealth Protection Here:Get Your Family Wealth Trust Blueprint Now – ILIT The Bigger Question What would happen if families stopped building alone? What would happen if communities focused on: instead of only survival? That question could change entire communities. Because the goal is not just making money. The goal is building systems strong enough to outlive us. #GroupEconomics #FamilyBank #BlackDollarAndCulture #GenerationalWealth #CommunityWealth #BlackWallStreet #CooperativeEconomics #Ownership #EconomicPower #ILIT #WealthBuilding #FamilyLegacy #BuildTogether #CommunityBank #FinancialFreedom Focus Keyphrase: What If 20 Families Started a BankSlug: what-if-20-families-started-a-bankMeta Description: Discover how 20 families pooling resources could create a powerful community wealth system through group economics, ownership, Family Banking, and ILIT wealth protection strategies.

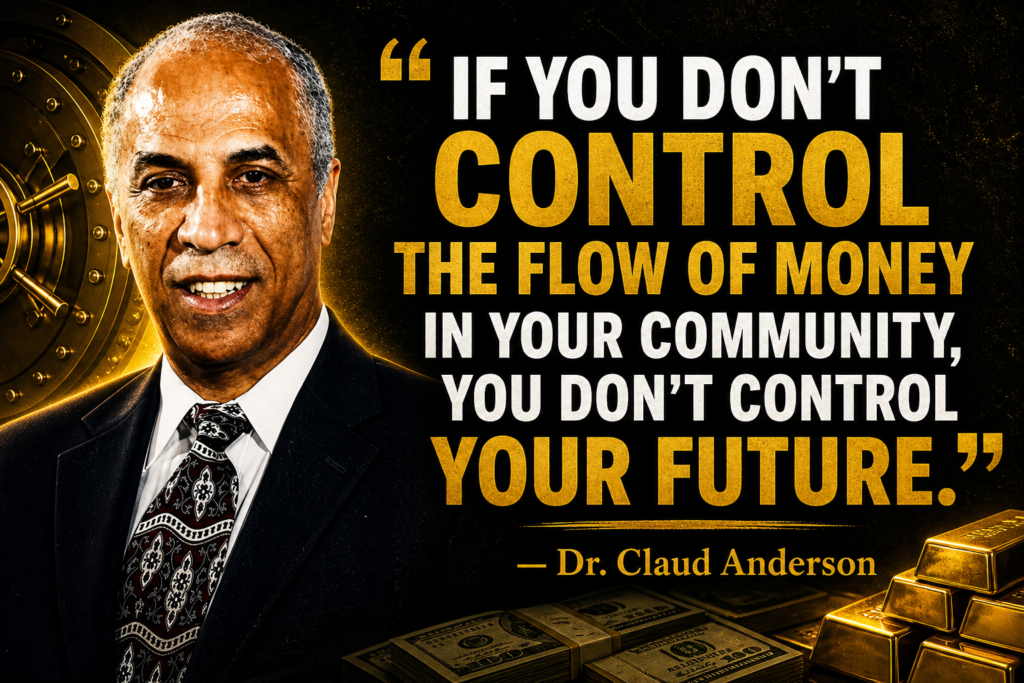

If You Don’t Control the Flow of Money… You Don’t Control Your Future (PowerNomics)

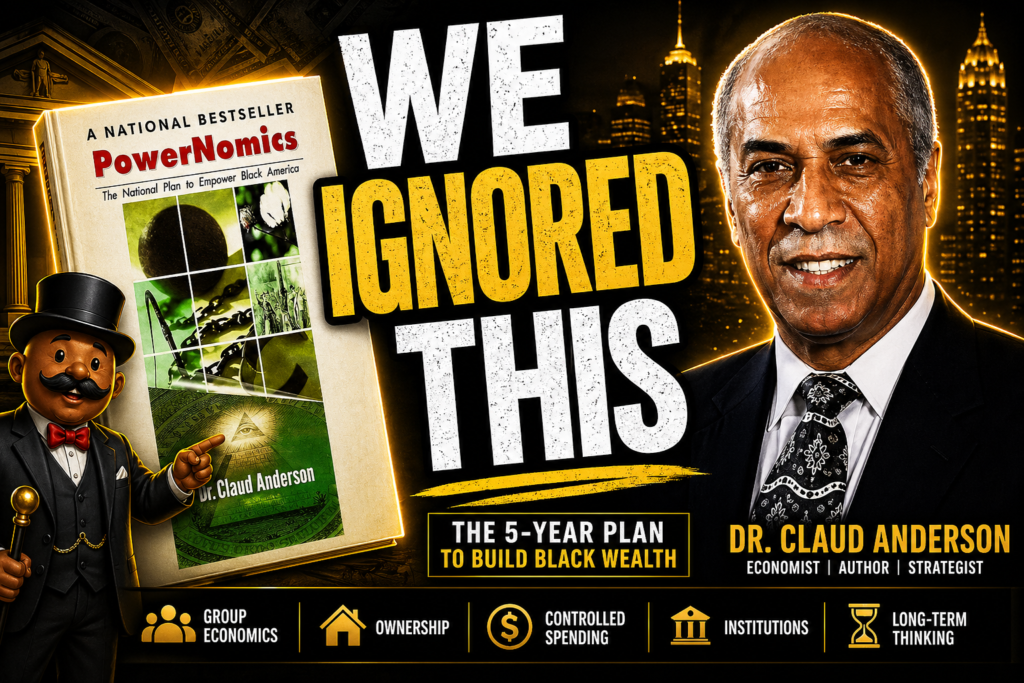

There are moments in history when the answers are already written… but ignored. In 1995, Dr. Claud Anderson released PowerNomics — not as motivation, not as theory, but as a blueprint. A structured plan to build economic power through one principle most people still overlook: group economics. And decades later, the question isn’t whether it works… it’s whether we’re finally ready to apply it. Because the issue was never a lack of talent, creativity, or ambition. The issue has always been structure. Money flows in… and flows right back out. Paychecks are earned, spent, and gone before they ever have the chance to circulate, multiply, or build anything lasting. That’s not an economy — that’s a pass-through system. And as long as money behaves that way, wealth will never take root. Group economics starts with a simple but uncomfortable truth: you cannot build wealth alone in a system designed around collective power. Every successful community understands this. Their money doesn’t just move — it moves with intention. It circulates internally. It supports businesses within the group. It hires within the group. It builds systems that reinforce itself before reaching outward. That’s not accidental. That’s design. When Dr. Claud Anderson laid out this framework, he wasn’t asking for support out of sympathy — he was outlining a strategy of survival and control. Because whoever controls the flow of money… controls the outcome. And when money leaves immediately, so does opportunity, ownership, and influence. Think about it in real terms. A dollar earned today can either disappear by tomorrow… or circulate five, six, seven times — creating jobs, sustaining businesses, and funding growth along the way. That’s the difference between spending and building. One is temporary. The other is intentional. But group economics requires a shift in thinking — from individual success to collective progress. It means asking different questions before every transaction: Who am I supporting? Where is this money going? What is this building? Because every dollar is a vote. And too often, those votes are cast without strategy. The blueprint is clear. First, money must circulate. Then, ownership must follow. Then institutions are built. And finally, legacy is secured. But without that first step — without group economics — everything else collapses before it ever begins. This is why so many efforts fail. People jump straight to ownership without circulation. They try to build institutions without a base. They aim for wealth without a system to sustain it. And when the foundation isn’t there, nothing holds. That’s what makes this conversation different. This isn’t about doing more. It’s about doing differently. Because once money begins to circulate, something powerful happens. Businesses stabilize. Networks form. Opportunities increase. And slowly, control begins to shift. Not overnight — but consistently. That’s how real economic power is built: quietly, strategically, and collectively. And that’s exactly why this message still matters today. Because the blueprint was never lost. It was just never fully applied. So the real question isn’t whether group economics works… It’s whether we’re finally ready to stop letting money pass through our hands — and start making it work for us. Start Building the System (Don’t Just Learn It) If this message resonates, the next step is structure — not just understanding. 👉 Build Your Internal Economy (Family Bank Starter System)https://stan.store/blackdollarandculture/p/the-family-bank-starter-system 👉 Protect & Pass Down Wealth (ILIT Trust Blueprint)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now Because building wealth is one thing… Keeping it — and passing it down — is everything. 🔁 Support the Movement 👉 Discover and support businesses that keep money circulating:https://blkcirculation.com 📊 FAQ: Group Economics & PowerNomics What is group economics?It’s the practice of circulating money within a community to build collective wealth, reduce dependency, and increase economic control. Why is group economics important?Because money that leaves immediately cannot multiply. Circulation is what turns income into wealth. What did Dr. Claud Anderson teach in PowerNomics?That economic power comes from structure — group economics, ownership, institutions, and long-term planning. Why hasn’t this been widely applied?Because most systems condition individuals to operate independently rather than collectively, weakening economic impact. 🔑 Final Thought They knew this in 1995. The blueprint didn’t change. The system didn’t change. The only thing left… is whether we will. #GroupEconomics #PowerNomics #ClaudAnderson #BlackWealth #GenerationalWealth #EconomicEmpowerment #Ownership #WealthBuilding #FinancialLiteracy #BlackBusiness #CommunityWealth #MoneyCirculation #FamilyBank #ILIT #WealthStrategy Group Economics PowerNomics group-economics-powernomics-1995-blueprint Discover Dr. Claud Anderson’s Group Economics blueprint from PowerNomics and learn how to build, circulate, and protect generational wealth today.

PowerNomics Explained: The 1995 Blueprint for Black Wealth We Still Haven’t Used

In 1995, a blueprint was laid out that most people never truly studied. Not because it was hidden.Not because it was complicated. But because it required something most people weren’t ready for: Discipline, structure, and long-term thinking. Dr. Claude Anderson didn’t speak in vague ideas. He didn’t deal in motivation. He laid out a system — one that explained exactly why wealth wasn’t sticking, and what it would take to change that. And if we’re being honest… The problem was never a lack of information. It was a lack of application. The Real Issue Was Never Just Money Most people think the problem is income. “If we just made more, everything would change.” But that’s not how wealth works. Dr. Anderson pointed to something deeper — something most people overlook: Control. You can make money and still be broke in the long run if you don’t control: If money comes in and immediately leaves, it doesn’t matter how much you earn. You’re not building wealth. You’re financing someone else’s. How Money Actually Builds Power Let’s slow this down and make it real. Imagine two different communities. Community A The money is gone within days. No ownership. No return. No growth. Community B Now that same dollar: It doesn’t just move. It multiplies. That’s the difference between spending and circulation. And that difference determines everything. Why Ownership Is the Foundation One of the clearest messages from PowerNomics is this: If you don’t own it, you don’t control it. That applies to: When you don’t own these, you are always operating inside someone else’s system. That means: You participate… but you don’t direct. And participation without ownership doesn’t build lasting wealth. The Hidden Trap: High Income, No Structure This is where a lot of people today get caught. There are more people making money now than ever before. But ask yourself: Because here’s the reality: You can have a high income and still leave nothing behind. Why? Because income without structure turns into: But not long-term power. Why Wealth Keeps Resetting Every Generation This is one of the most important parts of the conversation. A generation works hard. They buy a house.They save some money.They build something. Then life happens: And because there’s no structure: So the next generation… Starts over. That’s not bad luck. That’s a missing system. The Part PowerNomics Tried to Fix Dr. Anderson wasn’t just pointing out problems. He was trying to install a mindset shift: From: To: From: To: From: To: Because wealth isn’t about one person getting ahead. It’s about building something that continues after you’re gone. What This Looks Like in Real Life Let’s bring this down to something practical. Instead of thinking:“I made money this year.” The question becomes:“What system did I build this year?” That could mean: Because once systems are in place… Money starts working differently. This Is Where Most People Need to Get Serious A lot of people agree with these ideas. But agreement doesn’t change anything. Execution does. And execution requires: Because the default system is designed for money to leave your hands. You have to intentionally build something that keeps it. If You’re Ready to Move From Ideas to Structure This is where most people stop. They understand the concept… but don’t build the system. If you’re serious about applying what you just read, you need tools that actually help you implement it. 👉 Start building your internal system here:The Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 👉 Make sure what you build actually lasts:Get Your Family Wealth Trust Blueprint (ILIT)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now 👉 Understand the deeper historical context behind all of this:The First World Before Erasurehttps://stan.store/blackdollarandculture/p/the-first-world-before-erasure The Truth Most People Don’t Want to Say Out Loud The blueprint wasn’t missing. It wasn’t hidden. It was there. Since 1995. Clear. Direct. Actionable. So the real question now isn’t about awareness. It’s about accountability. What are you going to build with the information you already have? FAQ What is PowerNomics?A framework created by Dr. Claude Anderson focused on building wealth through ownership, group economics, and strategic control of resources. Why is ownership more important than income?Because ownership gives you control over assets, opportunities, and long-term wealth, while income alone is temporary. What is a Family Bank?A structured system where families pool and circulate money internally to fund opportunities and build wealth collectively. What is an ILIT and why does it matter?An Irrevocable Life Insurance Trust helps protect and transfer wealth efficiently, preventing assets from being lost through taxes or poor planning. #PowerNomics #BlackWealth #GroupEconomics #OwnershipMatters #GenerationalWealth #FamilyBank #FinancialStrategy #WealthBuilding #EconomicPower #BlackDollar Focus Keyphrase: PowerNomics Blueprint ExplainedSlug: powernomics-blueprint-explainedMeta Description: A deep breakdown of Dr. Claude Anderson’s PowerNomics blueprint and how ownership, circulation, and structure build real generational wealth.

10 Ways the System Blocks Wealth (And What to Do About It)

Let’s be real for a second. Most people aren’t broke because they’re lazy. They’re stuck because they were never shown how money actually works—and in many cases, the system is designed to keep it that way. Not in a conspiracy-theory way… but in a very practical, everyday way. The rules of money are there—but they’re not taught where most people spend their time: school, work, and even at home. So what happens? You play the game without knowing the rules. Let’s break down 10 real ways the system blocks wealth—and more importantly, how you move around it. 1. School Teaches You to Work, Not Build From a young age, you’re trained to follow instructions, meet deadlines, and aim for a “good job.” But there’s almost zero focus on ownership, investing, or building assets. What to do instead:Start learning money on your own terms. Study: Your real education begins after school ends. 2. The 9–5 Trap A job gives stability—but it also caps your time and income. You’re trading hours for dollars, and there’s only so many hours in a day. What to do instead:Keep your job if needed—but build something on the side: The goal isn’t to quit your job fast—it’s to outgrow it. 3. Taxes Hit Workers the Hardest Employees get taxed before they even see their money. Meanwhile, businesses and investors often get tax advantages. What to do instead:Learn how to legally reduce taxes by: Don’t just make money—learn how to keep it. 4. Credit Is Used Against You Instead of For You Most people use credit to survive—cars, clothes, emergencies—then get stuck in high-interest cycles. What to do instead:Use credit strategically: 5. Consumer Culture Keeps You Spending Everywhere you look, you’re being told to buy something. New phone, new car, new look. It’s designed to keep your money moving… just not toward you. What to do instead:Shift from consumer to owner: 6. Lack of Ownership Most people don’t own anything that produces income. No stocks, no businesses, no real estate—just bills. What to do instead:Start small, but start: Ownership is the real key to wealth. 7. Information Is Scattered and Confusing There’s so much financial information online—but it’s either too complex, too basic, or straight-up misleading. What to do instead:Stick to simple, proven principles: Don’t chase every trend—build a foundation. 8. Debt Is Normalized Debt isn’t always bad—but the way it’s pushed on people is dangerous. High-interest debt keeps you working just to stay afloat. What to do instead:Control your debt: 9. No Blueprint for Generational Wealth Most families pass down habits—not assets. So every generation starts from scratch. What to do instead:Become the blueprint: This is how cycles get broken. 10. Fear and Lack of Exposure If you’ve never seen wealth up close, it can feel out of reach. Fear of losing money keeps people from even starting. What to do instead:Expose yourself to new environments: Confidence comes from action—not waiting. Final Thoughts The system doesn’t reward people who just “work hard.” It rewards people who understand how money flows—and position themselves on the right side of it. Once you see that, everything changes. You stop chasing money…And start building systems that bring it to you. If you’re serious about taking control of your financial future, start building your own structure: 👉 The Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 👉 Get Your Family Wealth Trust Blueprint (ILIT)https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now These aren’t theories—these are tools to help you move differently with money and start thinking long-term. Hashtags (copy & paste):#BlackWealth #GenerationalWealth #FinancialFreedom #MoneyMindset #WealthBuilding #Ownership #InvestingBasics #FamilyBank #FinancialLiteracy #BuildAssets Focus Keyphrase: system blocks wealthSlug: system-blocks-wealthMeta Description: Discover 10 ways the system blocks wealth and learn practical steps to build financial freedom, ownership, and generational wealth starting today.

After Integration: Why Black Wealth Stalled — And What We Must Do Now

There was a moment in American history when the doors finally opened. Schools began to integrate. Businesses that once turned us away now allowed us to walk in. Opportunities that were once denied started to appear within reach. From the outside, it looked like progress.It looked like victory. But underneath that surface… something else was happening. Because while we were celebrating access, we were quietly losing control. Before integration, Black communities had no choice but to depend on themselves. And out of that necessity came something powerful—circulation. Black dollars moved through Black hands. Black doctors served Black families. Black teachers educated Black children. Black banks funded Black dreams. Entire ecosystems were built, not because it was trendy… but because it was required. Places like Tulsa’s Greenwood District—often called Black Wall Street—weren’t accidents. They were the result of forced unity, economic discipline, and a clear understanding: if we don’t build for ourselves, nobody will. But integration changed the direction of that energy. For the first time, we were allowed to spend freely outside of our communities. And understandably, many did. After generations of exclusion, the ability to go anywhere felt like freedom. But here’s the part nobody talks about enough: Access without ownership is not power. Because while we gained access to other systems… we slowly stopped investing in our own. The same dollar that once circulated multiple times within our neighborhoods began to leave almost immediately. Black-owned businesses, once the backbone of the community, started losing consistent support. Institutions we built out of necessity were now competing with systems that had far more resources, visibility, and capital. And over time, the shift became clear. We integrated into the economy…But we didn’t anchor ourselves within it. So instead of controlling wealth, we began participating in it. There’s a difference. Participation means you can spend money.Control means you can direct where it goes, how it grows, and who it benefits. And that difference is what we’re still feeling today. Now let’s be clear—this is not about going backwards. This is not about rejecting integration. This is about understanding what was lost… so we can rebuild it with intention. Because the real issue was never integration itself. The issue was that we integrated without a strategy. We entered larger systems without building strong systems of our own first. We pursued inclusion without securing ownership. And we adopted spending habits without maintaining economic discipline. And the result? We became some of the most influential consumers in the world…But not the most powerful owners. So the question becomes: What must we do now? Not emotionally.Not politically.But economically. Because wealth is not built through feelings—it’s built through systems. 1. Rebuild Internal Circulation (The Foundation) Every strong community has one thing in common: money flows within it before it flows out. Right now, the Black dollar leaves the community faster than almost any other group. That means even when money is earned, it doesn’t stay long enough to multiply. This is where intentionality comes in. Supporting Black businesses is not just about culture—it’s about economics. Every dollar spent internally creates jobs, strengthens businesses, and builds stability. And this is exactly where action meets solution. Because one of the biggest problems today isn’t willingness… it’s visibility. People want to support Black businesses.They just don’t always know where to find them. That’s why platforms like: 👉 https://blkcirculation.com …are so important right now. BLK Circulation is built to solve the discovery problem—connecting the community directly to Black-owned businesses so the dollar doesn’t just get earned… it gets recycled. Instead of money leaving immediately, it can now circulate intentionally. Discover. Support. Build. That’s how ecosystems are rebuilt. 2. Build Family Financial Systems (Not Just Income) Income alone doesn’t create wealth. Systems do. Most families operate financially as individuals—everyone earning, spending, and surviving on their own. But wealthy families think differently. They operate like institutions. That’s where the concept of a Family Bank comes in. Instead of sending interest to outside banks, families can create internal lending systems—funding businesses, covering emergencies, and keeping capital circulating within the family unit. This is how money starts to work for the family instead of constantly leaving it. 👉 Start building yours here:💰 Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 3. Protect Wealth Before You Build It One of the biggest mistakes people make is focusing only on making money… without protecting it. Because if wealth isn’t structured properly, it can disappear just as fast as it’s created—through taxes, legal issues, or lack of planning. This is where tools like trusts come in. An Irrevocable Life Insurance Trust (ILIT) allows families to pass down wealth efficiently, avoiding unnecessary taxation and ensuring the next generation actually benefits. 👉 Learn how to structure yours here:🛡️ ILIT Trust Blueprinthttps://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now 4. Shift From Consumer Identity to Owner Identity We’ve mastered influence. Music. Culture. Trends. Style. Language. But influence without ownership is rented power. The next level is ownership. Ownership of businesses.Ownership of land.Ownership of systems.Ownership of platforms. Because when you own, you don’t just participate in the economy—you shape it. 5. Think in Generations, Not Moments Everything changes when the mindset shifts from: “What can I do this year?”to“What can my family control in 30 years?” That’s how wealth is built. Not through one viral moment.Not through one paycheck.But through consistent systems that outlive the individual. The truth is… integration gave us access. But access alone was never the goal. Ownership is. Control is. Legacy is. And the next chapter won’t be defined by what we were allowed into… It will be defined by what we build, protect, and pass down. Because the real power was never just in being included. It’s in owning the system itself. Two families. Same income. Different mindset.One spends freely and hopes for the best.The other builds systems, protects assets, and circulates money intentionally. Ten years later, one is still working for money…The other has money working for them. The difference isn’t luck. It’s structure. If you’re ready to stop just participating in the economy—and start building

Why W-2 Workers Pay More Taxes (And How the System Was Designed That Way)

There’s a truth most people don’t realize until it’s too late: The more you follow the traditional path—get a job, earn a steady paycheck, work your way up—the more exposed you are to taxation. W-2 workers don’t just pay taxes.They pay the most consistent, unavoidable taxes in the system. And the people who understand this don’t rely on that structure alone. The Hidden Structure of W-2 Income When you earn income as a W-2 employee, your earnings are fully visible and automatically taxed. Before you receive your paycheck, multiple deductions have already been applied: You are taxed before you have the opportunity to allocate or structure your money. There is no control over timing.There is little control over deductions.There is no flexibility in how income is reported. How Wealth Is Taxed Differently Higher-net-worth individuals rarely rely on W-2 income as their primary source of earnings. Instead, income is structured through: This creates a different flow: Earn → Allocate → Deduct → Tax what remains Compared to: Earn → Taxed → Spend The difference is not income level alone.It is structure. The Advantage of Deductions and Control W-2 earners have limited access to meaningful deductions. Business owners and investors, on the other hand, can: Two individuals earning the same amount can end up with significantly different tax outcomes based solely on how their income is structured. The System Rewards Ownership This is often misunderstood as unfair, but it is more accurate to say the system is designed with a specific incentive: Ownership is rewarded. Those who: are given tools to reduce taxable exposure. W-2 income provides stability, but it offers the least amount of strategic flexibility. The Shift From Income to Structure The objective is not necessarily to abandon employment immediately. The objective is to begin building outside of it. The goal is not simply to earn more.It is to gain control over how money is earned, taxed, and deployed. Where the Family Bank Fits In A family bank system introduces internal control over capital. Instead of relying entirely on external lenders and institutions, families can: This shifts the focus from income to control and circulation. Get The Family Bank Starter System:https://stan.store/blackdollarandculture/p/the-family-bank-starter-system Protecting the Structure With a Trust Building wealth without protecting it creates exposure. Trust structures allow families to: Get Your Family Wealth Trust Blueprint (ILIT):https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now The Core Difference W-2 Earners: Structured Wealth: FAQ Do W-2 workers always pay more taxes?They typically have fewer tools to reduce taxes, which often results in a higher effective tax burden compared to structured income earners. Is a business required to reduce taxes?Not required, but it is one of the most effective ways to gain flexibility and access to deductions. Are trusts only for wealthy families?No. Many middle-income families can benefit from basic trust structures for protection and planning. Final Thought The system does not primarily reward effort.It rewards structure. Once that becomes clear, the focus shifts from working harder to building smarter systems. #BlackDollarCulture #WealthBuilding #FinancialEducation #TaxStrategy #GenerationalWealth #FamilyBank #TrustFund #Ownership #FinancialFreedom #AssetBuilding Focus Keyphrase: Why W-2 Workers Pay More TaxesSlug: why-w2-workers-pay-more-taxesMeta Description: Learn why W-2 workers often pay more taxes and how structured income through businesses, investments, and trusts can reduce tax exposure and build long-term wealth.

4 Ways to Pay Yourself First (And Build Real Wealth Before Bills Touch Your Money)

Most people get paid… and immediately start paying everyone else. Rent.Car note.Subscriptions.Debt. By the time they look up—there’s nothing left. That’s not an accident. That’s a system designed to keep you circulating money… instead of keeping it. Wealthy individuals don’t operate like that. They follow one simple rule: Pay yourself first. Before the world gets a dollar—you do. Here are 4 powerful ways to start doing that immediately. 1. Automatic Wealth Transfer (Before You See the Money) The easiest way to build wealth… is to remove emotion from the process. Set up an automatic transfer from your checking account to: The key is simple:You should never even see the money you’re saving. Because if you see it… you’ll spend it. Start with: This turns saving into a system—not a decision. 2. Pay Your Future Self Through Investments Saving money is good. But investing is what builds real wealth. Every time you get paid, allocate a portion to: This is how you move from:Working for money → Money working for you Even small amounts compound. Consistency beats intensity. 3. Build Your Family Bank First Most families:Go to the bank when they need money. Wealthy families:Are the bank. Instead of sending interest to outside institutions… You can: That means:Car loans, emergencies, business funding… All stay inside the family ecosystem. This is how wealth stops leaking. 4. Eliminate “Leftover Thinking” Most people save what’s left. Wealth builders invest first… and live on the rest. That mindset shift alone changes everything. Instead of saying:“I’ll save what I don’t spend…” Say:“I’ll spend what’s left after I build wealth.” That forces: The Real Shift Paying yourself first isn’t just about money. It’s about control. Control over: Because if you don’t prioritize yourself… The system will always prioritize itself. 💡 Final Thought You don’t build wealth by working harder. You build wealth by keeping more of what you earn—and putting it to work. 🚀 Call to Action If you’re serious about building something that lasts beyond you… 👉 Start your own financial system with my book:The Family Bank Starter Systemhttps://stan.store/blackdollarandculture/p/the-family-bank-starter-system 👉 And take it even further with asset protection and generational wealth strategy:Get Your Family Wealth Trust Blueprint Now – ILIThttps://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now Focus Keyphrase Pay Yourself First Wealth Strategy Slug pay-yourself-first-wealth-strategy Meta Description Learn 4 powerful ways to pay yourself first and build real wealth before bills take your money. Discover strategies used by wealthy individuals to grow financial freedom.