Why Your Paycheck Is the Least Important Part of Your Financial Life

Most people believe the key to financial security is earning more money. A bigger paycheck. A raise. A promotion. Another side hustle. And while income matters, this belief hides a dangerous truth: A paycheck is not wealth. It’s just a tool. If your entire financial plan depends on a paycheck continuing forever, you don’t have stability—you have exposure. And the system understands this far better than most people do. This is why some households earn six figures and still struggle, while others earn less but quietly build lasting wealth. Let’s break down what really matters. 1. A Paycheck Is Temporary by Design A paycheck depends on factors you don’t fully control: No matter how good the job is, a paycheck only exists as long as someone else allows it. Wealth, on the other hand, is designed to function without your daily presence. That’s the first major distinction most people are never taught. 2. Banks Don’t Respect Income — They Respect Structure Here’s something the system doesn’t advertise: Banks don’t analyze you emotionally.They analyze you structurally. They look at: A high income with no structure is treated as fragile.A modest income with assets, reserves, and discipline is treated as stable. This is why two people earning the same amount can be treated completely differently by financial institutions. 3. Income Is Fuel — Not the Destination Think of your paycheck like gasoline. Gas is necessary, but nobody confuses gas with the vehicle. Your paycheck should be used to: If all of your income is consumed by lifestyle, bills, and survival, then your paycheck is doing exactly what the system expects it to do: keep you running, but never arriving. 4. Ownership Outlives Effort Here’s the uncomfortable truth: You can work hard forever and still pass down nothing. Ownership is what survives: This is why wealthy families talk about control, not just cash. Cash gets spent. Control compounds. When income stops, ownership continues. 5. The Real Risk Is Dependency, Not Low Income Low income can be improved.High dependency is dangerous. If missing two paychecks would collapse your life, the issue isn’t how much you earn—it’s how exposed your financial structure is. True financial growth focuses on: Wealth isn’t loud. It’s resilient. 6. A Simple Shift That Changes Everything Instead of asking: “How can I make more money?” Start asking: “How can I make my money less necessary?” That question changes how you: This is where real financial freedom begins—not with hustle, but with intention. Final Thought Your paycheck is important—but it was never meant to be the foundation of your financial life. It’s a tool.A bridge.A starting point. The goal isn’t to earn forever.The goal is to build something that no longer requires permission. And once you understand that, you stop chasing money—and start designing stability. 📣 Keep the Conversation Going If this perspective shifted how you think about money, share this with someone who’s grinding but not building. Then explore more wealth-building strategies at Black Dollar & Culture, where we focus on ownership, structure, and legacy—because no one is coming to save us, and we don’t need them to. #BlackDollarCulture #FinancialLiteracy #WealthMindset #OwnershipEconomy #GenerationalWealth #FinancialFreedom #BuildTheBlock #QuietWealth #MoneyEducation #EconomicEmpowerment Focus Keyphrase: why paycheck is not wealthMeta Description: Most people chase bigger paychecks while ignoring ownership, structure, and control. Learn why income is the least important part of real wealth.Slug: why-your-paycheck-is-not-wealth

Money Rules the Rich Teach Their Kids (But Never Say Out Loud)

In certain households, money is never treated as a mystery. It’s not emotional, not dramatic, and not taboo. It’s discussed quietly, observed daily, and understood long before adulthood. Wealthy families rarely sit their children down and announce that they are about to teach them “the secrets of money.” Instead, they teach through behavior, structure, and repetition. By the time their children grow up, they don’t just earn money — they control it. One of the first unspoken lessons is that money is not the goal. In wealthy homes, money is framed as a tool. It exists to buy time, flexibility, and options. Children raised in these environments don’t chase money for validation. They learn that money is useful, but never emotional. This alone changes decision-making for life. When money loses its emotional charge, logic replaces impulse. Another quiet rule is that assets come before lifestyle. Wealthy parents do not rush to upgrade their lives every time income increases. Children grow up watching adults acquire businesses, equity, or income-producing assets before buying luxuries. The message isn’t spoken — it’s demonstrated. Lifestyle is something assets pay for, not something income is sacrificed to maintain. This creates patience and discipline that most people never develop. Jobs are also framed differently. In many households, a job is treated as the ultimate achievement. In wealthy families, a job is simply seed capital. Children hear conversations about using income to fund investments or ownership. Work is never positioned as identity. It’s positioned as leverage. As a result, wealthy children don’t grow up asking how to climb the ladder — they ask how to exit it. Ownership is the core principle behind everything. Cash is seen as temporary, while assets are permanent. Wealthy children grow up around deeds, shares, businesses, and partnerships. They understand early that ownership creates control, stability, and power. Saving money is respected, but hoarding cash is not glorified. Cash that isn’t deployed is seen as idle potential. Debt is another concept that’s handled with precision. In many families, debt is feared or misunderstood. In wealthy households, debt is treated like a tool that can either build or destroy depending on how it’s used. Children see debt used to acquire income-producing assets, never depreciating purchases meant for status. This distinction becomes second nature. Taxes are never framed emotionally either. Wealthy families don’t complain about taxes — they plan around them. Children overhear conversations about structure, strategy, and legal optimization. They learn early that taxes are not a punishment for success, but a penalty for ignorance. This understanding alone saves wealthy families millions over generations. One of the most powerful lessons is rarely spoken aloud: never sell an appreciating asset if you can borrow against it. Wealthy families hold onto assets and use loans for liquidity. This keeps ownership intact while allowing access to cash. Children raised with this mindset understand that selling stops compounding, while borrowing preserves it. Time is emphasized more than timing. Wealthy families teach patience by example. Children watch compounding happen slowly, then suddenly. They learn that starting early matters more than being perfect. Fast money loses its appeal when long-term growth proves unstoppable. Risk is not avoided — it’s managed. Wealthy parents don’t raise fearful children. They raise informed ones. Through diversification, insurance, and long-term planning, risk is reduced to something measurable rather than something terrifying. Children learn that avoiding risk entirely guarantees stagnation. Lifestyle inflation is quietly resisted. As income rises, expenses remain controlled. Children see adults live below their means while assets expand behind the scenes. This discipline protects future freedom and prevents wealth from leaking away unnoticed. Network is treated as an asset as well. Wealthy children grow up in environments where opportunity feels normal. Rooms matter. Conversations matter. Access changes outcomes faster than effort alone. This exposure shapes expectations for life. Perhaps the most important lesson is that wealth is taught at home. Schools are never relied upon to teach money. Children learn through participation, observation, and real-world involvement. Family discussions replace financial secrecy. Transparency replaces confusion. Finally, wealthy families value privacy. Quiet wealth is protected wealth. Flash is avoided. Attention is unnecessary. Power moves silently. Children learn that true wealth doesn’t need applause. By the time wealthy children become adults, the rules are already embedded. They don’t chase money. They deploy it. They don’t fear it. They control it. And that is the difference no one ever says out loud. Focus Keyphrase: money rules the rich teach their kids Meta Description: Explore the unspoken money rules wealthy families teach their children—covering assets, ownership, debt, taxes, discipline, and legacy thinking schools never explain. Slug: money-rules-the-rich-teach-their-kids

Black-Owned Businesses: Why Pouring Back Into the Community Is the Ultimate Power Move

This isn’t about charity. It’s about strategy.When Black-owned businesses reinvest into the communities that support them, they aren’t giving money away — they’re locking in longevity, loyalty, and leverage. History proves it. Modern data confirms it. And the future demands it. Before desegregation, before outside corporations flooded our neighborhoods, Black communities circulated the dollar dozens of times before it ever left. That circulation built schools, banks, hospitals, newspapers, and generational wealth. The collapse didn’t happen because the model failed — it happened because the system was disrupted. Here’s why pouring back in is not optional, but essential. 1. Community Investment Multiplies Business Survival Money spent locally doesn’t disappear — it cycles.When a Black business hires locally, sources locally, or sponsors locally, the community becomes economically invested in that business’s survival. That’s how you create customers who don’t just buy once — they defend your brand. • Local Jobs create Stable customers• Local Vendors reduce Costs and dependencies• Local Loyalty increases Lifetime value A supported community protects its own. 2. Wealth Circulation Builds Economic Immunity Every dollar that leaves the community weakens it.Every dollar that stays strengthens it. When Black businesses reinvest — through scholarships, youth programs, apprenticeships, or community real estate — they reduce dependency on outside systems that were never designed to protect us. This isn’t emotional. It’s mathematical. 3. Reinvestment Creates the Next Generation of Owners Communities don’t rise by consumption alone — they rise by ownership transfer. When successful Black businesses mentor youth, fund internships, or teach financial literacy, they aren’t just helping — they’re creating future partners, suppliers, and successors. Ownership is taught. Power is modeled. 4. Trust Is the New Currency In a world of ads, algorithms, and distractions, trust beats marketing. A business that visibly pours back into the community earns:• Word-of-mouth growth• Free brand ambassadors• Crisis-proof support People support what supports them. 5. Economic Power Is Political Power (Without Politics) You don’t need permission when you control resources. Communities with strong local businesses:• Fund their own initiatives• Solve problems internally• Negotiate from strength Reinvestment turns neighborhoods into economic blocs, not begging grounds. 6. The Blueprint Already Exists We don’t need new ideas — we need discipline and execution. From Greenwood (Black Wall Street) to Durham’s Black banking class, history shows that community-centered business models work when we commit to them long-term. The goal isn’t to escape the community — it’s to elevate it with you. The Bottom Line Black-owned businesses that pour back into the community don’t shrink — they compound. This is how legacies are built.This is how ecosystems form.This is how wealth stops leaking and starts circulating. 👉 Read more stories like this — and learn how ownership really works. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. #BlackOwnedBusiness #BlackWealth #EconomicPower #CommunityEconomics #BuyBlack #GenerationalWealth #BlackDollar #OwnershipMindset #BlackEntrepreneurs Focus Keyphrase: Black owned businesses community reinvestmentSlug: black-owned-businesses-community-reinvestmentMeta Description: Why Black-owned businesses pouring back into the community isn’t charity — it’s a proven strategy for wealth circulation, loyalty, and generational power.

Why Gold Protects Wealth When Markets Collapse

Markets don’t collapse overnight—they unravel quietly, then all at once. Long before the headlines turn red and panic becomes fashionable, confidence begins to erode beneath the surface. Liquidity tightens, assumptions fail, and investors realize—too late—that optimism was doing more work than fundamentals. When that confidence breaks, gold does what it has always done: it holds. Gold has never been an asset of excitement. It doesn’t trend on social media, it doesn’t promise outsized returns, and it doesn’t rely on narratives. It exists for moments of stress—when systems are questioned, currencies are diluted, and trust in leadership weakens. After surviving multiple market cycles, one lesson becomes unavoidable: markets reward growth, but wealth survives through protection. When stock markets collapse, it’s rarely because companies disappear overnight. It’s because valuations were built on fragile assumptions—cheap money, endless growth, stable geopolitics. Once those assumptions crack, repricing is swift and unforgiving. Gold doesn’t reprice on earnings calls or guidance forecasts. It responds to fear, uncertainty, and instability—the very conditions that define market collapses. Cash feels safe during chaos, but history exposes its weakness. Inflation quietly erodes purchasing power while governments respond to crises with stimulus, debt expansion, and money creation. Every collapse is met with liquidity, and liquidity always comes at a cost. Gold has no printing press. Its scarcity is real, which is why it preserves value when paper assets struggle to do the same. This is precisely why central banks hold gold. Not for tradition—but for credibility. When trust between nations weakens, gold becomes neutral ground. When debt loads grow uncomfortable, gold becomes reassurance. When currencies wobble, gold becomes stability. The same logic applies at the individual level. Another overlooked advantage of gold during market collapses is optionality. The most dangerous position an investor can be in during a downturn is forced selling. Gold provides liquidity without forcing the liquidation of productive assets at the worst possible moment. It buys time, and time is often the difference between recovery and permanent loss. Gold also behaves differently than most assets during crises. While correlations across markets tend to spike during panic, gold often diverges. It may not surge immediately, but it holds ground while others fall. That stability matters far more than aggressive upside when the goal is wealth preservation. The wealthy understand this distinction clearly. They don’t buy gold to outperform equities in bull markets. They hold it to survive bear markets. Gold is not designed to make headlines—it’s designed to protect capital when headlines turn ugly. History reinforces this lesson repeatedly. Empires rise and fall. Currencies are introduced, abused, and replaced. Financial systems evolve, break, and rebuild. Through every version of that cycle, gold remains relevant—not because it is old, but because it is independent. Gold does not replace businesses, real estate, or equities. It complements them. Think of it as structural support rather than decoration. You don’t admire it when times are calm, but without it, the foundation cracks under pressure. When markets collapse, emotions spread faster than facts. Gold does not react to emotion. It doesn’t panic, doesn’t promise, and doesn’t explain itself. It simply holds value while everything else explains why it can’t. That is why gold protects wealth—not through excitement, but through endurance. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. Focus Keyphrase:gold protects wealth Slug:why-gold-protects-wealth-when-markets-collapse Meta Description:When markets collapse and confidence disappears, gold has historically protected wealth. Learn why gold remains a powerful hedge during economic uncertainty.

Bessie Coleman: The Woman Who Refused to Stay Grounded

Bessie Coleman was born on January 26, 1892, in Atlanta, Texas, at the intersection of poverty, racism, and rigid limitation. She was the tenth of thirteen children born to George and Susan Coleman, a family of sharecroppers whose lives were shaped by the unforgiving realities of post-Reconstruction America. Cotton fields, long days, and scarce opportunity defined her early years. Education existed, but barely—one-room schoolhouses, worn textbooks, and interrupted learning whenever farm labor demanded it. Yet even in those conditions, Bessie showed an early hunger for knowledge, discipline, and something beyond the horizon. Her father eventually left the family, returning to Indian Territory in Oklahoma in search of a better life, while Bessie remained with her mother, helping raise her siblings and working the fields. Poverty was not an abstract concept to her; it was lived daily. But so was resilience. She excelled in school when she could attend, eventually saving enough money to enroll at Langston University in Oklahoma. Her time there was short—financial hardship forced her to withdraw—but the seed of ambition had already taken root. She would not accept a life dictated by circumstance. In her early twenties, Bessie moved to Chicago, joining the Great Migration of Black Americans seeking opportunity beyond the South. There, she worked as a manicurist, a job that placed her in close proximity to conversation, news, and stories from beyond her world. It was in a barbershop that her life took its decisive turn. She listened as Black men returned from World War I spoke of flying in Europe. They talked about airplanes, freedom, and skies that did not feel segregated. Her brothers, particularly one who had served in France, taunted her—telling her that French women could fly planes while American Black women could not. Instead of discouraging her, the insult ignited something irreversible. Bessie Coleman decided she would fly. The problem was America had no intention of letting her do so. Every aviation school she applied to rejected her. The rejections were absolute—no appeals, no alternatives. She was dismissed not for lack of intelligence or ability, but because she was both Black and a woman. In the early 20th century, flight was considered the domain of white men only. Rather than accept the denial, Bessie made a decision that defined her legacy: if America would not teach her, she would leave America. She enrolled in French language classes, saved her earnings meticulously, and gained sponsorship from influential Black newspapers, including the Chicago Defender. In 1920, she sailed to France. This alone was radical—an unmarried Black woman traveling abroad for professional training at a time when many Americans never left their home counties. In France, she trained at the Caudron Brothers’ School of Aviation, one of the most respected flight schools in the world. Flying in the 1920s was not glamorous. Planes were unstable, cockpits open to the elements, and crashes common. Training involved risk at every step. Bessie endured crashes, injuries, and intense discipline. But she persisted. On June 15, 1921, she earned her international pilot’s license from the Fédération Aéronautique Internationale, becoming the first Black woman in the world to do so—and one of the first Americans of any race to hold that distinction. When Bessie returned to the United States, her achievement should have made her a national hero. Instead, she encountered the same walls she had left behind. Airlines would not hire her. Commercial aviation opportunities were closed. Once again, racism tried to ground her ambitions. This time, she refused to stop moving forward. Bessie turned to barnstorming—performing aerial stunts at airshows across the country. Loop-the-loops, dives, figure-eights—she mastered them all. But her performances were not about spectacle alone. They were statements. Every time she climbed into a cockpit, she challenged the idea that Black people belonged only on the ground. She attracted massive crowds, especially in Black communities, where many had never seen an airplane up close, let alone one piloted by a Black woman. She was also uncompromising in her principles. Bessie refused to perform at venues that enforced segregated seating. If Black spectators were forced to enter through back gates or sit separately, she would not fly. This stance cost her income and opportunities, but she would not trade dignity for exposure. To her, flight symbolized freedom, and freedom could not exist alongside humiliation. Her vision extended far beyond stunt flying. Bessie dreamed of opening a flight school for Black aviators—men and women—so future generations would not have to leave the country to learn what she had fought to access. She spoke publicly about this goal, emphasizing education, discipline, and ownership of the skies. She wanted Black pilots, Black mechanics, Black instructors—an aviation ecosystem independent of exclusionary systems. Tragically, that dream was cut short. On April 30, 1926, in Jacksonville, Florida, Bessie Coleman boarded a plane for a practice flight ahead of an upcoming airshow. The aircraft was piloted by her mechanic, William Wills. Bessie was not wearing a seatbelt because she was scouting the terrain below, preparing for a parachute jump she planned to perform later. Mid-flight, the plane experienced a mechanical failure—later determined to be caused by a loose wrench lodged in the engine. The aircraft went into a sudden nosedive. Bessie was thrown from the plane at 2,000 feet and died instantly. She was 34 years old. Moments later, the plane crashed, killing Wills as well. Her death sent shockwaves through Black communities across the country. Thousands attended her funeral in Chicago. Leaders, activists, and ordinary people mourned not just the loss of a woman, but the loss of a future she represented. She died without ever opening the flight school she envisioned, without seeing the aviation doors she cracked open fully swing wide. Yet her impact did not end with her life. Bessie Coleman became a symbol—of courage without permission, of ambition without apology. Her legacy inspired future generations of Black aviators, including the Tuskegee Airmen during World War II. Pilots flew in her honor. Schools, clubs, and scholarships were named

Robert Reed Church: The Black Man Who Became the South’s First Millionaire After Slavery

They don’t teach this story in schools because it disrupts a lie that America has spent centuries protecting—the lie that Black people never built wealth on their own, never mastered systems, never owned power before it was taken from them. Robert Reed Church did all three. Born enslaved in Mississippi in 1839, Robert Reed Church entered the world as property. His mother was enslaved. His father was a white steamboat captain who never publicly claimed him but quietly ensured that Church learned something most enslaved people were denied—how money moved. By the time emancipation arrived, Church was no longer just free. He was prepared. While many newly freed Black Americans were pushed into sharecropping—a system designed to trap them in permanent debt—Church made a different decision. He went where money flowed: the Mississippi River. As a young man, he worked on steamboats, not just as labor but as a businessman. He learned routes. He learned trade. He learned leverage. And most importantly, he learned land. After the Civil War, Memphis was chaos. Disease, political instability, and racial violence made white property owners panic. During the yellow fever epidemics of the 1870s, thousands fled the city. Property values collapsed. White landowners sold prime real estate for pennies just to escape. Robert Reed Church saw opportunity where others saw collapse. With cash saved from years of disciplined work and investing, Church bought land—lots of it. Downtown Memphis. Beale Street. Commercial corridors. Not farmland. Not scraps. Prime urban real estate. While others speculated, he owned. By the 1880s, Church was the largest Black landowner in the South. By the 1890s, he was worth over one million dollars—making him the first Black millionaire in the South after slavery, at a time when lynchings were public entertainment and Jim Crow was tightening its grip. But Church didn’t just build wealth for himself. He understood something most wealthy people do: money without community is fragile. He invested heavily in Black Memphis. He built Church Park and Auditorium, one of the largest Black-owned entertainment venues in the country. It hosted concerts, political meetings, conventions, and speeches by leaders like Booker T. Washington. When Black people were locked out of public spaces, Church created their own. He financed Black businesses when banks refused. He backed schools when the state neglected them. He used his influence to protect Black institutions during periods of racial terror—not with speeches, but with ownership and political pressure. And then came 1892. That year, Memphis exploded with racial violence after the lynching of three successful Black businessmen. Many Black residents fled the city, fearing massacre. Again, white landowners sold. Again, Robert Reed Church bought. His wealth grew not from exploitation—but from discipline, timing, and understanding systems. Church also understood legacy. His son, Robert Reed Church Jr., became one of the most powerful Black political figures in America, helping found the NAACP and turning Memphis into a center of Black political organization. This was not accidental. This was design. Robert Reed Church died in 1912, but his blueprint remains painfully relevant today. He proved that Black wealth was never impossible—only interrupted. He proved that land ownership is power. He proved that economic independence is louder than protest. And he proved that when Black people are allowed—even briefly—to operate without sabotage, they build cities. They erased his name because his existence is evidence. Evidence that Black Wall Streets didn’t appear by accident.Evidence that wealth can be built even in hostile systems.Evidence that the problem was never Black ability—but white interference. Robert Reed Church didn’t beg for inclusion. He bought the ground beneath the system—and stood on it. SEO Elements Slug:robert-reed-church-first-black-millionaire-south Meta Description:The untold story of Robert Reed Church, the first Black millionaire in the South after slavery, who built wealth through land ownership, discipline, and economic independence in Memphis.

How a Roth IRA Can Make Your Family Rich (Not Just Comfortable)

Most families chase income.Wealthy families build systems. A Roth IRA is one of the most powerful—and most misunderstood—systems available to everyday people. Used correctly, it doesn’t just help you retire comfortably. It can quietly turn your household into a multi-generation wealth engine. Let’s break down exactly how. 1. A Roth IRA Grows Tax-Free Forever • Contributions are made with after-tax dollars• Investments grow tax-free• Withdrawals in retirement are 100% tax-free This matters because taxes are the silent killer of wealth.Every dollar that avoids taxation compounds faster—and compounding is how families get rich slowly, then suddenly. 2. Time Turns Small Contributions Into Large Outcomes • $6,500 per year sounds small• 30–40 years of compounding is massive• Growth beats hustle when time is on your side A family that starts early doesn’t need luck, crypto bets, or viral income. Time does the heavy lifting. 3. Roth IRAs Protect You From Future Tax Increases • No one knows future tax rates• Governments historically raise taxes• Roth IRAs lock in today’s tax rate forever This is wealth defense.You pay taxes once—on your terms—and never again. 4. You Can Pass a Roth IRA to Your Children • Roth IRAs can be inherited• Heirs receive tax-free growth• Funds can stretch across years This is how wealthy families move money forward without erosion. Not through income—but through ownership structures. 5. Roth IRAs Work Perfectly With Family Banks & Trusts • Roth IRAs pair well with trusts• They fit inside Family Bank strategies• They protect wealth from mismanagement This is how money stays in the family longer than one generation. 6. You Can Invest the Roth IRA—It’s Not a Savings Account • Stocks• ETFs• Index funds• Dividend assets The Roth IRA is a container, not an investment.What you put inside determines how powerful it becomes. 7. The Real Secret: It Teaches Discipline, Not Just Returns • Automatic investing• Long-term thinking• Delayed gratification Families who win financially think decades ahead. A Roth IRA trains that mindset quietly, year after year. 8. This Is How Rich Families Think Rich families don’t ask: “How much can I make this year?” They ask: “How do I protect and multiply money for the next 40 years?” A Roth IRA answers that question. Final Thought You don’t need millions to start acting wealthy.You need structures, time, and discipline. A Roth IRA isn’t flashy.It’s not loud.But it’s one of the cleanest tools ever created for turning income into legacy. 📌 Focus Keyphrase How a Roth IRA can make your family rich 🔗 Slug how-a-roth-ira-can-make-your-family-rich 📝 Meta Description Learn how a Roth IRA can quietly build tax-free, generational wealth for your family using time, discipline, and smart investing strategies.

The Cheapest Way to Start Investing With Just $5 (Yes, Really)

Most people believe investing is something you do after you make money.That belief alone has kept millions of people permanently on the sidelines. The truth is uncomfortable for the system—but powerful for you: Investing doesn’t start with wealth.Wealth starts with investing. And today, that journey can begin with just $5. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. 1. The Lie That Investing Is “Only for People With Money” For decades, investing was intentionally framed as something exclusive. You needed: This wasn’t accidental. When people believe investing is unreachable, they: The result?Generations trapped in a cycle where money passes through them, not works for them. But the rules quietly changed. Technology removed the gatekeepers—yet the old mindset remained. 2. What $5 Can Actually Buy You Today Thanks to fractional investing, you no longer need to buy an entire share of a company. You can buy a piece. That $5 can now purchase: This matters because ownership compounds, even in small amounts. While $5 in a savings account stays $5 (or loses value to inflation),$5 invested participates in growth. You’re no longer just holding money.You’re deploying it. 3. Why ETFs Are the Smartest Place to Start With $5 For beginners, the goal is not excitement.The goal is survival and consistency. That’s why Exchange-Traded Funds (ETFs) are ideal. ETFs: Instead of betting on one company, you’re betting on the system itself continuing to grow. This is not gambling.This is ownership. 4. The Real Power Isn’t the $5 — It’s the Habit Here’s what most people miss: The dollar amount matters far less than the behavior. When you invest $5: Small, repeated actions beat large, emotional decisions every time. Someone who invests $5 consistently will outperform someone who waits years for “the right time.” Because the market rewards time, not perfection. 5. A Simple $5 Investing Strategy That Actually Works This isn’t complicated. That’s the point. Step 1: Choose one broad-market ETFStep 2: Invest $5 weekly or bi-weeklyStep 3: Automate itStep 4: Ignore the noise No charts.No predictions.No panic. Over time, your money benefits from: You’re no longer guessing.You’re participating. 6. What NOT to Do With $5 Starting small doesn’t mean acting reckless. Avoid: Those strategies punish beginners and reward experience. $5 is not for chasing dopamine.It’s for building discipline and foundation. Wealth grows quietly before it grows loudly. 7. Why Waiting Is More Expensive Than Starting Small People often say:“I’ll invest when I make more.” But every year you wait: Time is the most expensive currency you own. Starting with $5 today beats starting with $500 five years from now. Because ownership rewards patience, not pride. 8. How This Connects to Generational Wealth Generational wealth doesn’t begin with inheritance.It begins with knowledge and repetition. When investing becomes normal: The amount grows later.The mindset must start now. This is how families quietly separate from the financial struggle most people accept as normal. 9. The Psychological Shift That Changes Everything Once you invest—even with $5—you cross a line. You stop asking:“How much does this cost?” And start asking:“What does this return?” That shift changes how you see: Ownership rewires thinking. And thinking shapes outcomes. 10. Final Truth Most People Never Hear You don’t start investing because you’re rich.You get rich because you start investing. The cheapest way to begin isn’t about money. It’s about deciding to own. Frequently Asked Questions Is investing $5 really worth it?Yes—because it builds habit, exposure, and discipline. The habit matters more than the amount. Is it better to save or invest $5?Emergency savings come first, but long-term growth requires investing. Saving alone does not build wealth. How often should I invest small amounts?Weekly or bi-weekly works best. Consistency beats timing. Can small investments really grow over time?Yes. Compound growth rewards time in the market, not size of the first deposit. Slug: cheapest-way-to-start-investing-with-5-dollarsMeta Description: Learn the cheapest way to start investing with just $5. Discover how small, consistent investing builds real wealth, ownership, and long-term financial freedom—even for beginners.

Why Millions of American Children Are Reading Below Grade Level — and How the System Failed Them

America is facing a crisis it doesn’t like to talk about because it exposes something deeper than test scores. Millions of children across the country are reading below grade level, and this is not a coincidence, a fluke, or the fault of parents who “didn’t try hard enough.” It is the predictable outcome of a system that stopped prioritizing literacy, accountability, and long-term outcomes—and replaced them with bureaucracy, shortcuts, and political comfort. Reading is not just another subject. Reading is the gateway skill. When children can’t read, they can’t fully access math, science, history, or even basic instructions. A child who struggles to read by third grade is statistically more likely to struggle for the rest of their academic life. By middle school, the gap widens. By high school, it calcifies. And by adulthood, it becomes an economic disadvantage that quietly follows them everywhere. This didn’t happen overnight. And it didn’t happen by accident. 1. The Alarming Reality No One Can Spin Away Across the United States, standardized assessments and independent studies show a staggering number of children reading below grade level. In some districts, the majority of students are behind. In others, the numbers are so normalized that failure has become expected instead of urgent. What’s worse is that many students are being promoted to the next grade without mastering basic reading skills. This practice—often justified as protecting self-esteem or avoiding stigma—does the opposite. It guarantees long-term struggle by delaying intervention until it’s too late to be easy. Social promotion doesn’t solve literacy gaps. It hides them. 2. How the Education System Let This Happen The modern American education system is overloaded with initiatives but underloaded with fundamentals. Over the past few decades, reading instruction shifted away from proven, structured phonics-based methods toward experimental approaches that assumed children would “naturally” pick up reading through exposure. That assumption was wrong. Many schools deprioritized explicit reading instruction, reduced time spent on foundational literacy, and failed to train teachers adequately in evidence-based methods. Add overcrowded classrooms, underpaid educators, and inconsistent curriculum standards across states, and the result is predictable: uneven outcomes and widespread reading failure. The system optimized for graduation rates and optics—not mastery. 3. Who This Failure Hurts the Most Systemic failure never lands evenly. Children from working-class families, low-income households, and historically marginalized communities are hit the hardest. When schools fail to teach reading well, families with resources compensate with tutors, private programs, and supplemental learning. Families without those resources are told to “trust the system.” That trust is expensive. Black children, in particular, are disproportionately affected—not because of ability, but because of access. When literacy instruction fails early, it limits academic tracking, reduces confidence, and narrows future opportunities. The result is a pipeline from poor literacy to limited career options that has nothing to do with intelligence and everything to do with neglect. 4. Technology Didn’t Save Reading — It Distracted From It Tablets, apps, and digital learning tools were sold as solutions. In reality, they often replaced direct instruction instead of supporting it. Screens do not teach children how to decode words, build vocabulary, or comprehend complex text without guidance. Reading is a human skill learned through repetition, feedback, and structure. No app replaces an adult who knows how to teach it correctly. The system mistook convenience for progress. 5. Why Waiting on Reform Is a Risk Families Can’t Afford Educational reform moves slowly. Children grow quickly. Every year a child remains behind in reading is a year that compounds difficulty across all subjects. Hoping the system “fixes itself” before your child reaches critical academic milestones is a gamble with long odds. Families who understand this are no longer waiting. 6. What Parents Must Do Now (Even If the System Doesn’t) This is the hard truth: literacy has become a family responsibility, not just a school one. That doesn’t mean parents failed. It means parents must adapt. Families can: Reading is the foundation of independence. A child who reads well can teach themselves anything else. Final Thought America doesn’t have a child intelligence problem. It has a systems problem. When millions of children can’t read at grade level, the issue isn’t effort—it’s design. Systems produce exactly the outcomes they are built for. And right now, this system is producing underprepared readers at scale. Families who recognize this early have an advantage. Not because they are better—but because they refuse to outsource their children’s future to a system that already showed its limits. Literacy is power.And power can’t be postponed. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. Focus Keyphrase: children reading below grade level in AmericaSlug: why-american-children-reading-below-grade-levelMeta Description: Millions of American children are reading below grade level. This article explains how the education system failed them and what families must understand now.

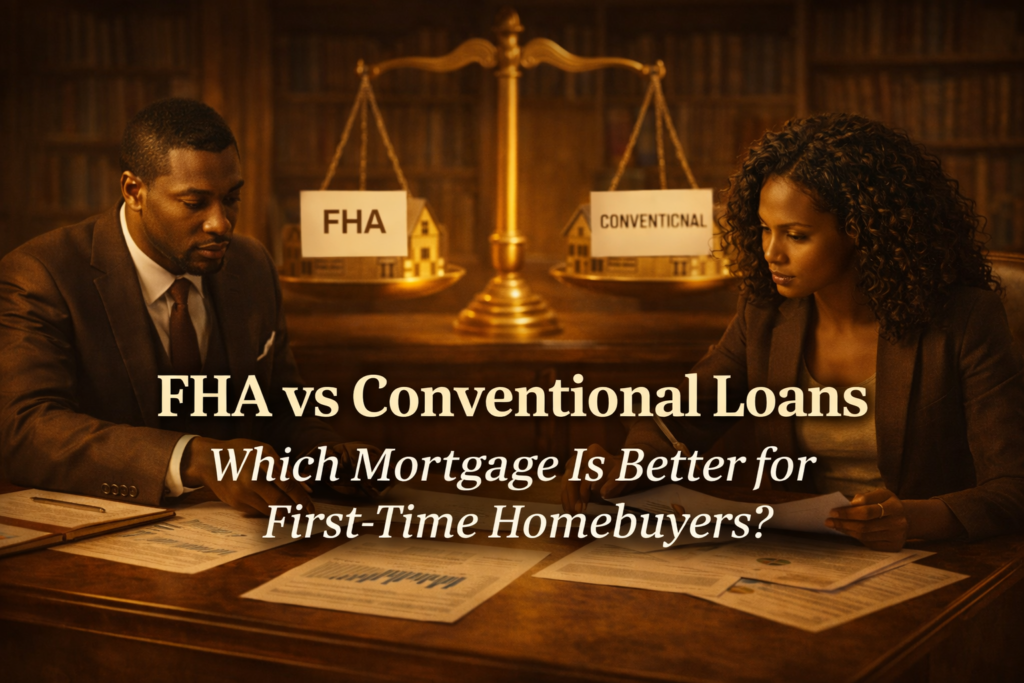

FHA vs Conventional Loans: Which Mortgage Is Better for First-Time Homebuyers?

Buying your first home isn’t just a milestone — it’s a financial fork in the road. Choose the right mortgage, and you build equity faster, save thousands in interest, and gain flexibility. Choose the wrong one, and you overpay for years without realizing why. Two options dominate the conversation for first-time buyers: FHA loans and conventional loans. Both can get you into a home. Only one may be right for your situation. Let’s break them down clearly. 1. What an FHA Loan Is (Plain English) An FHA loan is a mortgage backed by the Federal Housing Administration. It was designed to help buyers with lower credit scores or limited savings qualify for a home. Key traits: FHA loans are often marketed as the “starter” mortgage — and for some buyers, they are. 2. What a Conventional Loan Is A conventional loan is not backed by the government. It’s issued by private lenders and typically rewards borrowers with stronger credit and stable finances. Key traits: Conventional loans are often overlooked by first-time buyers who assume they don’t qualify — even when they do. 3. Down Payment Requirements Compared This is where most buyers focus first — sometimes too much. The difference is smaller than most people think. A lower down payment helps you get in the door, but it doesn’t tell the full cost story. 4. Credit Score Requirements This is where FHA loans shine — but with a tradeoff. If your credit is still recovering, FHA may be the bridge.If your credit is solid, conventional often wins long-term. 5. Mortgage Insurance: The Hidden Cost Most Buyers Miss This is the most important difference — and the one that costs people the most money. FHA Mortgage Insurance (MIP) Conventional Private Mortgage Insurance (PMI) Over time, FHA insurance can cost tens of thousands more than conventional PMI. 6. Monthly Payment Comparison Even with a similar home price: What looks cheaper upfront isn’t always cheaper long-term. 7. Long-Term Wealth Impact (This Is Where Strategy Matters) Homeownership isn’t just about getting approved — it’s about building equity efficiently. Conventional loans usually: FHA loans are better viewed as: Many smart buyers start FHA and later refinance into conventional — if they plan correctly. 8. Which Loan Is Better for First-Time Homebuyers? Here’s the honest answer: FHA May Be Better If: Conventional May Be Better If: The “best” loan isn’t universal.It’s situational. 9. The Biggest Mistake First-Time Buyers Make Most buyers ask: “Which loan gets me approved fastest?” Smarter buyers ask: “Which loan builds wealth with the least friction?” Approval is temporary.Mortgage costs are permanent. Final Thought FHA loans help people get in the game.Conventional loans help people win the game. The right move isn’t rushing into a mortgage — it’s choosing one that fits your credit today and your goals tomorrow. The difference can be tens of thousands of dollars — and years of progress. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these lessons alive — lessons they never wanted us to learn. Focus Keyphrase: FHA vs Conventional Loans for first-time homebuyersSlug: fha-vs-conventional-loans-first-time-homebuyersMeta Description: Compare FHA vs conventional loans to see which mortgage is better for first-time homebuyers, including down payments, credit requirements, mortgage insurance, and long-term costs.