The Significance of December 19, 1865: A Pivotal Moment in Black History

Understanding the 13th Amendment The 13th Amendment, ratified on December 6, 1865, represents a critical juncture in American history, particularly in the advancement of civil rights for African Americans. It abolished slavery and involuntary servitude, except as punishment for a crime, thereby laying the groundwork for future legislative and social reforms aimed at achieving equality. The Amendment’s roots can be traced back to the broader context of the Civil War, where the fight against the Confederacy was also a fight against the institution of slavery itself. The passage of the 13th Amendment was championed by numerous abolitionists, politicians, and leaders of the Union. Key figures such as President Abraham Lincoln played a pivotal role, utilizing his influence to promote emancipation as a war measure. During the war, the moral imperative to end slavery gained traction, causing a significant shift in public opinion. This advocacy was set against a backdrop of intense political strife, as various factions within Congress debated the future of the Union and the fate of millions of enslaved individuals. The political climate of the time was marked by a struggle for power between pro-slavery and anti-slavery factions. The Republican Party, having emerged from the abolitionist movement, found its platform centered around the idea of freedom for all individuals. The Civil War solidified the urgency for the passage of the 13th Amendment, as the Union victory prompted discussions about the reconstruction of the nation and the status of freed slaves. Ultimately, the amendment’s ratification marked a significant change in the constitutional fabric of the United States, signaling a new era in which African Americans could begin to claim their rights as free citizens. The Implications of Freedom without Economic Power The abolition of slavery in 1865 marked a significant milestone in American history, ushering in a new era of freedom for African Americans. However, this newfound freedom often came with the harsh reality of economic disenfranchisement. While individuals were freed from the shackles of bondage, they were not provided with the resources or opportunities necessary to thrive in a competitive economy. The transition from slavery to freedom did not automatically translate into equality, particularly in terms of economic power. Many newly freed African Americans found themselves without land, capital, or education, which severely limited their ability to achieve financial independence. The promise of land grants and economic support was largely unmet, leaving them to navigate a landscape marred by systemic barriers. The practice of sharecropping emerged as a dubious solution, perpetuating a cycle of debt and poverty. In this system, African Americans would rent land from white landowners in exchange for a share of the crop, often leading to exploitation and barely subsistence living. Moreover, labor exploitation was rampant, as many freed individuals were relegated to low-paying jobs that offered no room for advancement. Economic opportunities were scarce, as racial discrimination restricted access to skilled employment and education. Such circumstances perpetuated economic disparities that would haunt Black communities for generations. Without access to economic resources, the struggle for true freedom continued, affecting the social fabric and future prospects of African Americans. This intersection of freedom with economic power underscores an essential understanding of Black history, highlighting the ongoing challenges faced by these communities in their pursuit of equality. Legacy of the 13th Amendment in Modern America The passage of the 13th Amendment on December 6, 1865, marked a significant turning point in American history by signaling the formal abolition of slavery. However, the legacy of this pivotal amendment extends far beyond its initial intent, as it continues to influence discussions on racial inequality and social justice in contemporary society. While the formal institution of slavery ended, various systemic issues, such as mass incarceration and economic disparities, have arisen that disproportionately affect African Americans. Mass incarceration has emerged as a leading concern in discussions surrounding the 13th Amendment. Many advocates argue that although the amendment abolished slavery, it inadvertently allowed for a new form of servitude through prison labor. The current penal system, with its disproportionate representation of Black individuals, raises critical questions about the true nature of freedom. Activists cite the over-policing of African American communities and harsh sentencing laws as modern manifestations of racial discrimination that demand attention and reform. In addition to incarceration, economic empowerment remains a significant challenge for African Americans. Despite legal advancements since the 13th Amendment, there are ongoing disparities in wealth and employment opportunities. Efforts to address these disparities, such as advocating for fair hiring practices and equitable access to education, are essential steps towards achieving true equality. Grassroots movements led by organizations focused on civil rights, such as Black Lives Matter, have emerged in response to these challenges, further emphasizing the need for systemic change. In examining the enduring legacy of the 13th Amendment, it is clear that the fight for freedom and equality for African Americans is far from complete. Historical and contemporary issues intersect to create a complex landscape that requires continued advocacy and policy reform to ensure that the promise of the 13th Amendment is fully realized. Only through persistent efforts can the ideals of freedom and equality be truly achieved for all citizens. Commemoration and Reflection on December 19 December 19, 1865, marks a significant turning point in Black history, representing a time when African Americans began to gain momentum in their fight for freedom and equality. This date is not only a historical milestone but also serves as a reminder of the ongoing struggles faced by Black communities. In the years since, various educational initiatives have been instituted to ensure that this pivotal moment is recognized and remembered. Schools, colleges, and community organizations often host events on this day to foster awareness and understanding of its importance. Black leaders and movements play a crucial role in advocating for economic justice, promoting the significance of this date as a cornerstone of freedom. These leaders often remind us that the fight for equality extends beyond the abolition of slavery, encompassing various facets of social justice, including access

What Happens to the Black Community When Black Men Marry Outside the Race?

For decades, conversations around Black men dating or marrying outside the race have been framed emotionally — accusations, defensiveness, and surface-level debates about “preference.” But very little attention is paid to the structural impact of these choices on the Black community as a whole. This article isn’t about policing love.It’s about understanding how marriage functions as an economic and social institution — and what happens when participation in that institution becomes uneven. According to Pew Research Center, about 24% of Black male newlyweds married outside their race, compared to roughly 9% of Black female newlyweds. That imbalance alone creates long-term consequences that go far beyond individual relationships. Let’s break down what that actually means. Marriage in America is the primary mechanism through which wealth is pooled, protected, and passed down. Two incomes combine, assets are acquired jointly, homes are purchased, businesses are built, and children inherit both financial and social capital. When a Black man marries within the Black community, those economic benefits are statistically more likely to circulate within Black households, Black neighborhoods, and Black institutions. When a significant portion of Black men marry outside the race, a growing share of Black male income, assets, and future earnings becomes structurally anchored outside the Black community. This isn’t about intentions. It’s about where capital compounds over time. The effect multiplies across generations. Children are the carriers of legacy — not just DNA, but culture, identity, and economic direction. Research consistently shows that children spend more time in the primary custodial household, usually the mother’s. Cultural identity, social networks, and future relationship patterns tend to follow that environment. Over time, this leads to fewer Black-identified households, fewer Black family units, and weaker continuity in culture, economics, and community affiliation. The imbalance also directly affects Black women. Because Black men marry outside the race at nearly three times the rate of Black women, the available marriage pool shrinks. This contributes to lower marriage rates among Black women, delayed family formation, and a higher prevalence of single-parent households. That matters because two-parent households, regardless of race, statistically accumulate more wealth, experience less economic stress, and provide more stability for children. This isn’t a moral judgment — it’s a demographic reality. There’s also a political and economic dimension that often goes unspoken. Marriage influences where people live, which schools children attend, where families invest, how they vote, and which businesses they support. When high-earning Black men — especially athletes, entertainers, and executives — marry outside the race, their economic footprint, political influence, and philanthropy frequently become integrated into other communities rather than anchored in Black ones. That’s why the impact feels larger than the numbers suggest. While celebrities make up a small percentage of Black men, they represent an outsized share of visible Black wealth. When those resources exit the community, the loss is amplified — not symbolically, but materially. Still, it’s important to be precise: interracial marriage itself is not the problem. The real issue is a combination of low overall Black marriage rates, weak asset protection, and the absence of a coordinated strategy for retaining and compounding Black wealth. When out-marriage occurs alongside declining in-marriage and minimal financial planning, the community experiences capital leakage instead of circulation. If Black men married Black women at higher rates, protected assets through prenups and trusts, and intentionally reinvested in Black institutions, interracial marriage would not register as a crisis. It would simply be a personal choice within a strong, resilient system. The uncomfortable truth is this: marriage is not just about love. It is an economic contract, a wealth-building vehicle, and a power-transfer mechanism. When participation in that system becomes uneven, the effects are predictable — and they compound. Understanding that reality doesn’t require blame. It requires strategy. Focus Keyphrase: Black love and wealth Slug: black-men-interracial-marriage-impact-black-communityMeta Description: A data-driven look at how Black men marrying outside the race affects Black wealth, family formation, and long-term community power.

Why Millions of American Children Are Reading Below Grade Level — and How the System Failed Them

America is facing a crisis it doesn’t like to talk about because it exposes something deeper than test scores. Millions of children across the country are reading below grade level, and this is not a coincidence, a fluke, or the fault of parents who “didn’t try hard enough.” It is the predictable outcome of a system that stopped prioritizing literacy, accountability, and long-term outcomes—and replaced them with bureaucracy, shortcuts, and political comfort. Reading is not just another subject. Reading is the gateway skill. When children can’t read, they can’t fully access math, science, history, or even basic instructions. A child who struggles to read by third grade is statistically more likely to struggle for the rest of their academic life. By middle school, the gap widens. By high school, it calcifies. And by adulthood, it becomes an economic disadvantage that quietly follows them everywhere. This didn’t happen overnight. And it didn’t happen by accident. 1. The Alarming Reality No One Can Spin Away Across the United States, standardized assessments and independent studies show a staggering number of children reading below grade level. In some districts, the majority of students are behind. In others, the numbers are so normalized that failure has become expected instead of urgent. What’s worse is that many students are being promoted to the next grade without mastering basic reading skills. This practice—often justified as protecting self-esteem or avoiding stigma—does the opposite. It guarantees long-term struggle by delaying intervention until it’s too late to be easy. Social promotion doesn’t solve literacy gaps. It hides them. 2. How the Education System Let This Happen The modern American education system is overloaded with initiatives but underloaded with fundamentals. Over the past few decades, reading instruction shifted away from proven, structured phonics-based methods toward experimental approaches that assumed children would “naturally” pick up reading through exposure. That assumption was wrong. Many schools deprioritized explicit reading instruction, reduced time spent on foundational literacy, and failed to train teachers adequately in evidence-based methods. Add overcrowded classrooms, underpaid educators, and inconsistent curriculum standards across states, and the result is predictable: uneven outcomes and widespread reading failure. The system optimized for graduation rates and optics—not mastery. 3. Who This Failure Hurts the Most Systemic failure never lands evenly. Children from working-class families, low-income households, and historically marginalized communities are hit the hardest. When schools fail to teach reading well, families with resources compensate with tutors, private programs, and supplemental learning. Families without those resources are told to “trust the system.” That trust is expensive. Black children, in particular, are disproportionately affected—not because of ability, but because of access. When literacy instruction fails early, it limits academic tracking, reduces confidence, and narrows future opportunities. The result is a pipeline from poor literacy to limited career options that has nothing to do with intelligence and everything to do with neglect. 4. Technology Didn’t Save Reading — It Distracted From It Tablets, apps, and digital learning tools were sold as solutions. In reality, they often replaced direct instruction instead of supporting it. Screens do not teach children how to decode words, build vocabulary, or comprehend complex text without guidance. Reading is a human skill learned through repetition, feedback, and structure. No app replaces an adult who knows how to teach it correctly. The system mistook convenience for progress. 5. Why Waiting on Reform Is a Risk Families Can’t Afford Educational reform moves slowly. Children grow quickly. Every year a child remains behind in reading is a year that compounds difficulty across all subjects. Hoping the system “fixes itself” before your child reaches critical academic milestones is a gamble with long odds. Families who understand this are no longer waiting. 6. What Parents Must Do Now (Even If the System Doesn’t) This is the hard truth: literacy has become a family responsibility, not just a school one. That doesn’t mean parents failed. It means parents must adapt. Families can: Reading is the foundation of independence. A child who reads well can teach themselves anything else. Final Thought America doesn’t have a child intelligence problem. It has a systems problem. When millions of children can’t read at grade level, the issue isn’t effort—it’s design. Systems produce exactly the outcomes they are built for. And right now, this system is producing underprepared readers at scale. Families who recognize this early have an advantage. Not because they are better—but because they refuse to outsource their children’s future to a system that already showed its limits. Literacy is power.And power can’t be postponed. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. Focus Keyphrase: children reading below grade level in AmericaSlug: why-american-children-reading-below-grade-levelMeta Description: Millions of American children are reading below grade level. This article explains how the education system failed them and what families must understand now.

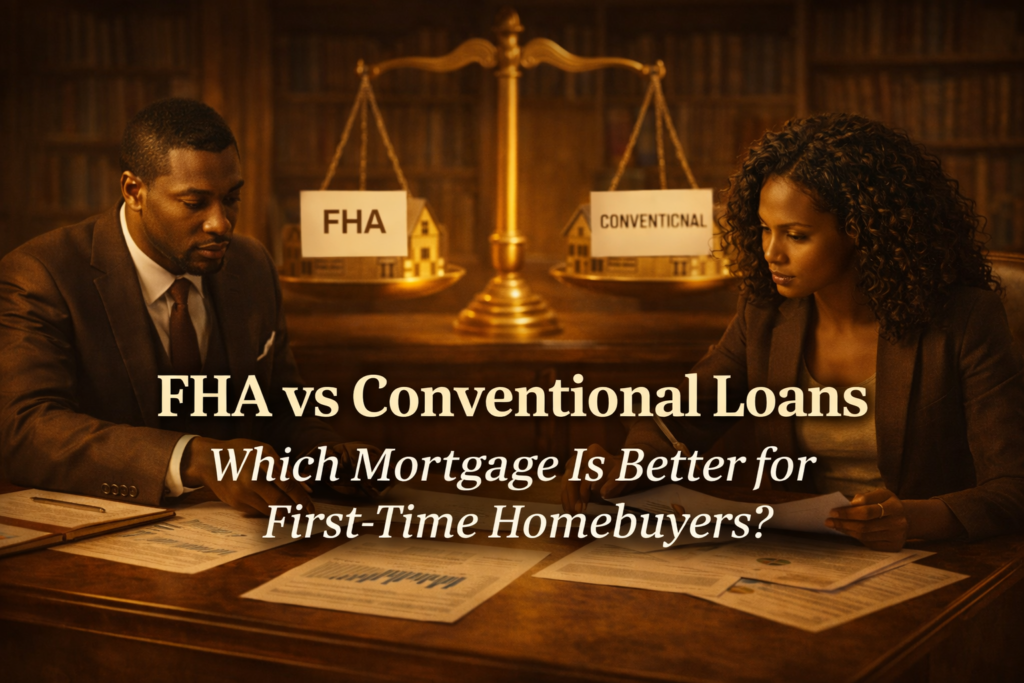

FHA vs Conventional Loans: Which Mortgage Is Better for First-Time Homebuyers?

Buying your first home isn’t just a milestone — it’s a financial fork in the road. Choose the right mortgage, and you build equity faster, save thousands in interest, and gain flexibility. Choose the wrong one, and you overpay for years without realizing why. Two options dominate the conversation for first-time buyers: FHA loans and conventional loans. Both can get you into a home. Only one may be right for your situation. Let’s break them down clearly. 1. What an FHA Loan Is (Plain English) An FHA loan is a mortgage backed by the Federal Housing Administration. It was designed to help buyers with lower credit scores or limited savings qualify for a home. Key traits: FHA loans are often marketed as the “starter” mortgage — and for some buyers, they are. 2. What a Conventional Loan Is A conventional loan is not backed by the government. It’s issued by private lenders and typically rewards borrowers with stronger credit and stable finances. Key traits: Conventional loans are often overlooked by first-time buyers who assume they don’t qualify — even when they do. 3. Down Payment Requirements Compared This is where most buyers focus first — sometimes too much. The difference is smaller than most people think. A lower down payment helps you get in the door, but it doesn’t tell the full cost story. 4. Credit Score Requirements This is where FHA loans shine — but with a tradeoff. If your credit is still recovering, FHA may be the bridge.If your credit is solid, conventional often wins long-term. 5. Mortgage Insurance: The Hidden Cost Most Buyers Miss This is the most important difference — and the one that costs people the most money. FHA Mortgage Insurance (MIP) Conventional Private Mortgage Insurance (PMI) Over time, FHA insurance can cost tens of thousands more than conventional PMI. 6. Monthly Payment Comparison Even with a similar home price: What looks cheaper upfront isn’t always cheaper long-term. 7. Long-Term Wealth Impact (This Is Where Strategy Matters) Homeownership isn’t just about getting approved — it’s about building equity efficiently. Conventional loans usually: FHA loans are better viewed as: Many smart buyers start FHA and later refinance into conventional — if they plan correctly. 8. Which Loan Is Better for First-Time Homebuyers? Here’s the honest answer: FHA May Be Better If: Conventional May Be Better If: The “best” loan isn’t universal.It’s situational. 9. The Biggest Mistake First-Time Buyers Make Most buyers ask: “Which loan gets me approved fastest?” Smarter buyers ask: “Which loan builds wealth with the least friction?” Approval is temporary.Mortgage costs are permanent. Final Thought FHA loans help people get in the game.Conventional loans help people win the game. The right move isn’t rushing into a mortgage — it’s choosing one that fits your credit today and your goals tomorrow. The difference can be tens of thousands of dollars — and years of progress. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these lessons alive — lessons they never wanted us to learn. Focus Keyphrase: FHA vs Conventional Loans for first-time homebuyersSlug: fha-vs-conventional-loans-first-time-homebuyersMeta Description: Compare FHA vs conventional loans to see which mortgage is better for first-time homebuyers, including down payments, credit requirements, mortgage insurance, and long-term costs.

How Black Americans Can Build Generational Wealth by Buying Assets During Economic Downturns

When the economy falls, most people freeze. The wealthy move. Every major fortune in American history was built during moments of fear—recessions, crashes, and downturns when prices were low and competition was scared. Economic downturns don’t destroy wealth. They transfer it. The question isn’t whether opportunity exists. The question is who is positioned to act. Assets don’t disappear in downturns. They get discounted. When markets fall: This is why the wealthy say, “Buy when there’s blood in the streets.” Not because they celebrate pain—but because pricing reflects emotion, not value. 2. The Assets That Matter Most During Downturns Not everything is worth buying just because it’s cheaper. Focus on assets that recover and compound. High-Priority Assets: Wealth is built by acquiring productive assets, not collectibles. 3. Cash Positioning Is the Real Advantage Downturns reward liquidity. Wealthy buyers prepare before crashes by: This allows them to act without panic. Cash doesn’t make you rich—but it lets you buy things that do. 4. Why Credit Access Separates Buyers From Spectators In downturns, banks tighten lending for most people— but extend favorable terms to strong borrowers. That’s why credit preparation matters: Credit is leverage. And leverage, used correctly, multiplies opportunity. 5. The Historical Pattern Black Families Must Understand History is clear: From land after the Civil War… to housing after 2008… to stocks after 2020… The tragedy wasn’t lack of opportunity. It was lack of access, preparation, and education. That’s changing now. 6. Ownership Beats Income Every Time Jobs pay bills. Ownership builds balance sheets. During downturns: This is why wealthy families prioritize what they own, not just what they earn. 7. What Stops Most People From Buying When It Matters The barriers are rarely financial. They’re psychological. Common blockers: The market doesn’t reward confidence. It rewards preparation. 8. A Simple Wealth-Building Playbook for Downturns You don’t need perfection. You need structure. Repeat this cycle across generations—not quarters. 9. Why This Moment Matters More Than Most America has entered a period of: These windows don’t stay open long. Those who move now build foundations. Those who hesitate pay premiums later. Final Thought The wealthy don’t wait for certainty. They wait for value. Economic downturns don’t signal the end of opportunity. They announce its arrival—quietly, briefly, and without warning. Those who understand this build legacies. Those who don’t fund them. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these lessons alive — lessons they never wanted us to learn. Focus Keyphrase: Black Americans build generational wealth during economic downturns Slug: how-black-americans-build-generational-wealth-economic-downturns Meta Description: Learn how Black Americans can build generational wealth by buying assets during economic downturns, when prices are lower and long-term opportunities are greatest.

Cleopatra VII: The Wealthiest Queen Rome Ever Feared

History remembers Cleopatra VII as a lover, a seductress, a woman whose power supposedly came from beauty and manipulation. That version of her story is convenient. It’s also a lie. Cleopatra VII was not dangerous because of romance. She was dangerous because she controlled one of the richest economies on Earth at the exact moment Rome was starving for resources, legitimacy, and money. Empires do not smear women they consider harmless. They rewrite the stories of rulers who threaten them. When Cleopatra took the throne of Egypt in 51 BCE, she inherited more than a crown. She inherited an economic machine that had fed civilizations for centuries. Egypt was not simply a kingdom; it was the financial backbone of the Mediterranean world. Its grain fields along the Nile supplied food to Rome’s swelling population. Its ports controlled trade routes between Africa, the Middle East, and Europe. Its treasuries held gold, silver, and state reserves accumulated over generations. Cleopatra did not stumble into power. She was trained from childhood to manage it. Unlike many rulers of her era, Cleopatra spoke multiple languages fluently, including Egyptian, Greek, and Latin. This was not a cultural flex; it was a strategic weapon. She could negotiate directly with merchants, diplomats, and military leaders without translators who diluted meaning or leaked information. She understood trade, taxation, logistics, and statecraft. Cleopatra ruled Egypt not as a figurehead but as a chief executive of a sovereign economic power. Rome, by contrast, was drowning in ambition and debt. Its military campaigns were expensive. Its political elite fought constantly for dominance. Its population depended heavily on Egyptian grain to avoid famine and unrest. Cleopatra knew this. She understood leverage better than most men who sat in the Roman Senate. Control the food, and you control the empire that eats it. When Julius Caesar entered her story, it was not romance that drew Cleopatra to him; it was survival and strategy. Egypt faced internal power struggles and Roman interference. Aligning with Caesar stabilized her throne and protected Egypt’s autonomy. In return, Rome gained access to Egypt’s resources under negotiated terms rather than outright conquest. Cleopatra used diplomacy to buy time, preserve sovereignty, and keep Egypt independent in a world where Rome swallowed kingdoms whole. After Caesar’s assassination, Cleopatra aligned with Mark Antony, not as a love-struck queen but as a ruler securing military protection and political balance. Together they controlled enormous territory, trade routes, and naval power. At their height, Cleopatra and Antony governed lands that rivaled Rome’s influence. This was not scandal; it was geopolitics. Rome did not panic because Cleopatra was charming. Rome panicked because she was effective. What followed was not merely a military conflict but a propaganda war. Octavian, later known as Augustus, understood that Rome could not admit it feared a foreign Black queen who commanded wealth, loyalty, and economic leverage. So he reframed the narrative. Cleopatra became painted as immoral, manipulative, and decadent. Antony was portrayed as weak and corrupted by foreign influence. This narrative justified Rome’s aggression and masked the truth: Rome crushed Egypt not to save morality, but to seize resources. After Cleopatra’s death, Egypt was absorbed into the Roman Empire. Its treasuries were looted. Its grain supply was nationalized for Rome’s benefit. The wealth Cleopatra once controlled now fed Roman dominance for generations. And just like that, history shifted its tone. Cleopatra’s intelligence was erased. Her financial mastery was ignored. Her leadership was reduced to gossip. But facts do not disappear simply because empires prefer myths. Cleopatra VII ruled one of the richest states in human history. She controlled food, trade, gold, language, and diplomacy with precision. She understood that power is not loud; it is organized. And that is why Rome destroyed her image after destroying her kingdom. They could defeat her militarily, but they could not allow future generations to understand what she truly represented: a sovereign ruler who proved that wealth, intelligence, and strategy are far more threatening than swords. Cleopatra’s legacy is not romance. It is a lesson. Those who control resources shape the world, and those who challenge empires rarely get fair biographies. History often belongs to the victors, but wealth always leaves a trail. And if you follow the money, the grain, and the power, you find Cleopatra VII exactly where Rome feared her most — at the center of the economic world. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. Focus Keyphrase: Cleopatra VII wealth and power Slug: cleopatra-vii-wealth-power-rome Meta Description: Cleopatra VII was not just a queen but a powerful economic strategist who controlled Egypt’s wealth, trade, and grain supply—making her one of the most feared rulers Rome ever faced.

How the Wealthy Use Credit Cards to Build Wealth (And Why Most People Stay Broke With Them)

Most people are afraid of credit cards. The wealthy are afraid of using them wrong. That difference alone explains why one group drowns in debt…and the other quietly turns plastic into power. Credit cards are not the problem.Lack of structure is. Used incorrectly, credit cards trap you.Used correctly, they become leverage, protection, and a record of trust. Let’s break down how wealthy people actually use them — and why it works. 1. The First Rule: Wealthy People Never Use Credit Cards as Extra Money This is where most people fail immediately. Poor mindset: “I’ll pay it off later.” Wealthy mindset: “I already have the money — this is about timing and benefits.” Wealthy people treat credit cards as: If the money isn’t already accounted for, the card doesn’t get used. That’s discipline — not luck. 2. Credit Cards Are Used for Cash Flow Control, Not Consumption Wealthy people care about when money leaves more than how much leaves. Credit cards allow them to: That delay may seem small — but over years, it compounds. Money that stays liquid longer stays useful longer. 3. The Wealthy Use Rewards as a Rebate, Not a Bonus Most people chase points. Wealthy people earn rebates on spending they were already going to do. That means: Cash back, points, and travel perks aren’t “free money.”They’re efficiency rewards. Sir Wealthington would say: “If you must spend, make the system pay you back.” 4. Why Wealthy People Love Charge Cards and High-Limit Cards High-limit cards aren’t about flexing. They’re about utilization ratios. Here’s the quiet advantage: The wealthy don’t max cards.They keep balances strategically small relative to limits. This signals stability — and lenders respond accordingly. 5. Credit Cards as a Shield (Fraud, Liability, and Disputes) Cash has no protection. Debit cards expose your actual money. Credit cards?They create distance between you and risk. Wealthy people use cards because: Protection matters when assets grow. 6. How Businesses Use Credit Cards to Scale For entrepreneurs and investors, credit cards become: Used properly, they help businesses: Again — structure beats emotion. 7. Why Minimum Payments Keep People Poor The minimum payment is not a kindness.It’s a profit strategy. Wealthy people either: They do not: Interest is what you pay when discipline is missing. 8. The Credit Profile Is the Real Asset Wealthy people understand something most don’t: Your credit profile is a reputation system. It affects: Credit cards are simply the training ground. Used correctly, they prove: “This person can be trusted with capital.” 9. Sir Wealthington’s Rule on Credit Cards Sir Wealthington doesn’t hate credit cards. He hates confusion. He would say: “Credit cards don’t make you wealthy.But they expose whether you already have control.” Cards reward discipline.They punish impulse. And the system never forgets which one you chose. Final Thought (Read This Slowly) The wealthy don’t ask:“Can I afford the payment?” They ask:“Does this strengthen or weaken my position?” Credit cards are neither good nor bad. They are honest. They reveal who plans…and who reacts. ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these lessons alive — lessons they never wanted us to learn. Focus Keyphrase: how the wealthy use credit cards to build wealthSlug: how-the-wealthy-use-credit-cards-to-build-wealthMeta Description: Learn how wealthy people use credit cards to build wealth, manage cash flow, earn rewards, and strengthen their financial position without falling into debt.

What Is an ILIT (Irrevocable Life Insurance Trust) — And Why the Wealthy Never Skip This Step

Most people think life insurance is about death. The wealthy know it’s about control. An ILIT — Irrevocable Life Insurance Trust — is one of the most powerful wealth-preservation tools in existence, yet most families never hear about it until it’s too late… usually at a funeral, right before the government shows up with its hand out. This isn’t theory.This is how dynasties protect money, avoid estate taxes, and pass wealth cleanly — without begging the system for permission. 🎥 Watch This First (This short video explains why ILITs are one of the most misunderstood — and most powerful — tools for generational wealth.) Go Deeper:This article explains what an ILIT is.My ILIT Blueprint eBook walks you through how to structure one, avoid costly mistakes, and use life insurance as a private family bank.👉 Get the ILIT Blueprint here https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now 1. What an ILIT Actually Is (Plain English) An ILIT is a legal trust that owns your life insurance policy instead of you. That one shift changes everything. When the trust owns the policy: Translation:The money skips the government’s toll booth and goes straight to your family. 2. Why the Wealthy Use ILITs (And Most People Don’t) Here’s the quiet truth no one explains clearly: Life insurance payouts can become taxable if you own the policy yourself. When you do: When an ILIT owns the policy: This is why wealthy families don’t “hope things work out.” They design outcomes. If you want the exact structure wealthy families use, the full breakdown is inside my ILIT Blueprint eBook.👉 Access the ILIT Blueprint https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now 3. How an ILIT Works (Step-by-Step) Here’s the clean breakdown: No probate.No estate tax exposure.No chaos. Important: Most ILIT failures happen during setup.The ILIT Blueprint eBook explains trustee selection, funding rules, and the three-year lookback, so you don’t accidentally destroy the benefits.👉 Download the ILIT Blueprint https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now 4. Why “Irrevocable” Is the Price of Power “Irrevocable” scares people because it means: But that’s exactly why it works. The IRS only respects separation when it’s real.No loophole cosplay. No fake distancing. You trade flexibility for protection — and wealthy families make that trade gladly. 5. ILIT vs Naming a Beneficiary (This Is Where People Lose Wealth) Naming a beneficiary feels responsible. Using an ILIT is strategic. With only a beneficiary: With an ILIT: One is convenient.The other is built to last generations. 6. How ILITs Create Generational Wealth (Not Just a Payout) An ILIT isn’t just about receiving money — it’s about how money is released. You can design rules like: That prevents wealth from disappearing the moment emotions run high. Wealth without structure disappears.Wealth with structure multiplies. 7. Why ILITs Matter Especially for Black Families Let’s be honest. More Black wealth is lost to: …than to bad investments. An ILIT does something radical:It turns life insurance into a private family bank, not a public transaction. No courtrooms.No GoFundMe funerals.No confusion about “who gets what.” Just execution. This is why I created the ILIT Blueprint — to help families stop reacting and start building financial infrastructure.👉 Get the ILIT Blueprint here https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now 8. Who Should Seriously Consider an ILIT You should consider an ILIT if: This isn’t just for the wealthy. It’s for the intentional. 9. Common ILIT Mistakes to Avoid Avoid these at all costs: An ILIT done wrong is expensive paperwork. An ILIT done right is a fortress. Final Thought (Read This Twice) The wealthy don’t ask:“How much life insurance do I need?” They ask:“Who controls the money when I’m gone?” An ILIT answers that question before emotions, courts, or taxes get involved. That’s not insurance. That’s power. Want the playbook?If this article changed how you think about life insurance, the ILIT Blueprint eBook shows you how to turn knowledge into action.👉 Secure the ILIT Blueprint https://stan.store/blackdollarandculture/p/get-your-family-wealth-trust-blueprint-now ❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth. Every article you read helps keep these lessons alive — lessons they never wanted us to learn. Focus Keyphrase: ILIT Irrevocable Life Insurance TrustSlug: what-is-an-ilit-irrevocable-life-insurance-trustMeta Description: Learn what an ILIT (Irrevocable Life Insurance Trust) is, how it works, and why wealthy families use it to avoid estate taxes, protect assets, and build generational wealth.

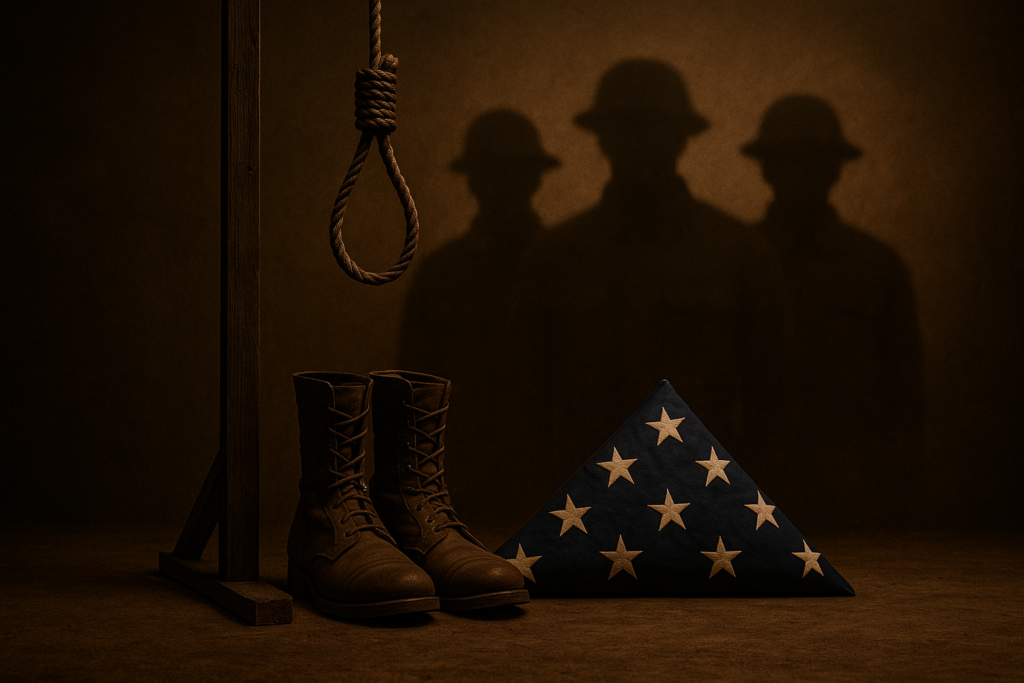

The 13 Buffalo Soldiers of the Houston Riot- A Dark Chapter in Black U.S. Military History

When the sun rose over Houston, Texas, on August 23, 1917, the Black soldiers of the 24th Infantry Regiment—men known with pride as Buffalo Soldiers—had already endured weeks of verbal abuse, beatings, threats, and relentless harassment by the city’s police force. These men were veterans, disciplined and decorated, trained to protect the nation overseas, yet they found themselves unprotected on American soil. Stationed in a Jim Crow city that treated Black people with open hostility, they faced a constant barrage of violence from officers who saw their uniforms not as symbols of honor, but as targets. On this day in Black History—December 11—we revisit the darkest moment that followed: the mass execution of thirteen of these soldiers after the Houston Riot of 1917, the largest mass execution of American troops in U.S. history and a chilling example of justice denied. The tension started long before the riot. Houston police would beat Black soldiers for walking on the wrong sidewalk, arrest them without cause, and assault Black women in front of them. One afternoon, police violently attacked a Black woman in the neighborhood. When a soldier stepped in to defend her, he was beaten and arrested. Later that same day, a Black military policeman was assaulted, shot at, and jailed when he tried to investigate the incident. Rumors spread through the camp that he had been killed. Fear mixed with anger, creating a storm no one could stop. Chaos erupted when soldiers, believing their comrade dead and fearing an imminent white mob attack, armed themselves to protect one another. Shots were fired in the dark. Panic ruled the city. When the smoke cleared, the Army responded not with investigation or fairness, but with swift punishment meant to appease Houston’s white leadership. Nearly 150 Black soldiers were rounded up and put on trial. They faced an all-white panel of officers, no legal representation, and no true chance to defend themselves. Witnesses contradicted one another, evidence was missing, and many of the accused had never even fired a weapon. Yet the verdict came with chilling speed: death. On December 11, 1917, before sunrise, thirteen Black soldiers were marched to a gallows built overnight. They sang hymns as they walked. Some prayed. Others looked to the sky. All maintained their innocence. Hooded and bound, they died as martyrs of a nation that demanded their loyalty but denied them dignity. For decades, this story was buried—quieted in textbooks, ignored by military historians, and dismissed as a “riot” rather than the desperate reaction of men cornered by racial terror. But as scholars revisited the case, the truth resurfaced: the trials were fundamentally unfair, the soldiers denied constitutional rights, and the rush to execution was driven by racism, pressure, and fear. The Army kept their graves unmarked for 70 years. It wasn’t until recent decades that their names were restored and their innocence acknowledged, marking a slow but powerful correction in history. These men were not criminals—they were victims of a system designed to break them. Yet this moment also revealed something deeper about Black resilience in America. Even after witnessing blatant injustice, Black troops continued to serve in World War I, World War II, Korea, Vietnam, and beyond. They fought for a country that didn’t fight for them because they believed in a future where freedom would eventually match the ideals written on paper. The story of the 13 Buffalo Soldiers forces us to face an uncomfortable truth: America has often punished its most loyal defenders when those defenders were Black. But remembering their names, their courage, and their sacrifice becomes an act of reclamation. It is a reminder that our history is not defined by oppression alone, but by the unstoppable determination of a people who refused to disappear. Today, we honor the thirteen men who walked to the gallows with dignity and faith, believing that someday the truth would set them free. Today, that truth is spoken aloud. ❤️ Support Independent Black MediaBlack Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth.Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. #BlackHistory #TodayInBlackHistory #BuffaloSoldiers #HoustonRiot1917 #24thInfantry #MilitaryInjustice #BlackHeroes #AmericanHistory #HiddenHistory #BlackDollarAndCulture #BDCHistory Keyphrase: Buffalo Soldiers Houston RiotSlug: buffalo-soldiers-houston-riot-december-11Meta Description: On December 11, 1917, thirteen Black Buffalo Soldiers were executed after an unjust trial following the Houston Riot. This long-form BD&C narrative reveals their true story, their courage, and America’s harshest military injustice. Most Americans never learned this story—but on December 11, thirteen Black soldiers were executed in silence after one of the most unjust trials in U.S. history. Click to uncover the truth.

How to Turn $25 a Week Into Real Wealth (Even on a Low Income)

❤️ Support Independent Black Media Black Dollar & Culture is 100% reader-powered — no corporate sponsors, just truth, history, and the pursuit of generational wealth.Every article you read helps keep these stories alive — stories they tried to erase and lessons they never wanted us to learn. 1. Why $25 a Week Is More Powerful Than You Think Most people underestimate small money because they only look at the number today — not what it becomes tomorrow. Wealth is built like a snowball: the earlier you start rolling it, the bigger it becomes. When you invest $25 weekly, you’re building three things at once: And here’s the truth:Wealth doesn’t start with a big amount — it starts with consistency. Even millionaires start with habits, not income. 2. What $25 a Week Looks Like Over Time If you invest $25 every week into a simple index fund (like VOO, SPY, or QQQ): This is how people with low incomes still retire with wealth:They automate their money and let time do the heavy lifting. 3. The Mindset Shift That Changes Everything The goal isn’t the $25. The goal is the identity you build: Once you master this mindset, you can scale the amount later. Wealth begins internally long before it shows up externally. 4. Where to Put Your $25 (Beginner-Friendly) Here are the safest, simplest places to start: ✅ 1. High-Yield Savings Account (HYSA) Perfect for beginners building the habit. ✅ 2. Index Funds (SPY, VOO, QQQ) Best long-term wealth builders. ✅ 3. Fractional Stocks Own pieces of major companies for as little as $1. ✅ 4. ETFs for Beginners Diversified, low-risk, and beginner-proof. You don’t need to be rich to invest.You need discipline — not dollars. 5. Why Building Wealth on a Low Income Matters When our community learns to turn small money into big power, everything changes: This is why BD&C exists — to show you what schools, banks, and the system never taught you. Wealth starts with a decision.And you can make that decision today with just $25. Slug: turn-25-a-week-into-real-wealth Meta Description:Turn just $25 a week into real wealth. Learn how even low-income earners can build long-term assets through small, consistent investing and smart money habits. how to turn $25 a week into real wealth Slug: turn-25-a-week-into-real-wealth Meta Description (155 characters): Learn how to turn just $25 a week into real long-term wealth. Even on a low income, you can build assets, invest smarter, and start your wealth journey today.